Quick Take on Tesla Q119 Deliveries: Yes, They Were Bad

Q1 Deliveries Tracked My Below Market Estimates, And That's Not All The Bad News

Tesla (TSLA) finally reported first-quarter production and delivery numbers late Wednesday night and, sure enough, results came in closer to my below-market estimates and trailed management guidance and market consensus (see my report Tesla’s Weak QTD Deliveries Signal March Expectation Madness).

Tesla also admitted it delivered half of its total deliveries for the entire quarter in the last nine days of March, blaming "challenges encountered" for delays in getting cars to buyers in Europe and China.

But even adding cars "in transit" doesn't cover the shortfall versus guidance and market expectations.

It also doesn't ease investors' concerns about cooling demand for Model 3 in the US, or the alarming drop-off in sales for Models S and X, well, everywhere.

Elon Musk was the only one laughing.

Tesla traditionally reports quarterly numbers for deliveries and production early in the morning a day or so after the quarter closes, so analysts and investors expected to hear something by Tuesday morning. Instead, Tesla was, without explanation, late, and later, and later.

There was little reason to expect good news after such a calamitous quarter, which included stunning sales declines, multiple rounds of price cuts and layoffs, a momentous change in sales strategy both ill-conceived and poorly executed, and ominous liquidity pressures worsened by hefty debt payments due and delayed financing for an expensive new plant in Shanghai already under construction.

Oh, and CEO Elon Musk is scheduled to be in court tomorrow for the hearing over whether he should be held in contempt for violating his settlement in October with the SEC for securities fraud.

What could go wrong? It's Tesla, so...everything. (See Tesla Bonds Go Boom, Tesla - Now We Know The Y, But Not the How, Tesla’s Plan B 2.0; Y Not, Tesla’s New Plan: Buy Before You Try, Tesla: Truth and Consequences, and Tesla: Shanghai Surprise.)

So after keeping the world waiting for two days, Tesla announced Wednesday morning, not first quarter delivery and production numbers but instead that it would host "Autonomy Investor Day" in two weeks to promote new capability (make that ease and/or aggregate growing concerns) with its problematic Autopilot:

“Today, we’re beginning to roll out our latest version of Navigate on Autopilot for a more seamless active guidance experience. In this new version, drivers will now have the option to use Navigate on Autopilot without having to confirm lane changes via the turn stalk. Here’s how it works:

In the Autopilot settings menu, a driver can press the Customize Navigate on Autopilot button which will now display three additional settings – Enable at Start of Every Trip, Require Lane Change Confirmation, and Lane Change Notification. Through the Enable at Start of Every Trip setting, Navigate on Autopilot can be set to automatically turn on each time a driver enters a navigation route. Once enabled, anytime a driver is on a highway and uses Autopilot with a location plugged into the navigation bar, the feature will be on by default. If a driver selects ‘No’ to Require Lane Change Confirmation, lane changes will happen automatically, without requiring a driver to confirm them first.”

Short take: the car will be able to change lanes without the driver's permission.

This comes amid burgeoning controversy over several fatal accidents when Tesla's autopilot malfunctioned (see William Keating 's latest report "Tesla. Autopilot Safety Claims Roundly Debunked As Deafening Silence Follows Latest Fatality"). Recently the CEO of Volvo Cars Hakan Samuelsson warned that it is,

“Irresponsible” to put autonomous vehicles on the road if they were not sufficiently safe, because that would erode trust among the public and regulators. “We have a responsibility and everybody who’s in this business has that responsibility because otherwise, you’re going to kill a technology that might be the best lifesaver in the history of the car.

Some carmakers have launched partially autonomous systems that can control steering and braking while on highways. But overstating the abilities of these cars will lead to “over-reliance” by consumers and cause accidents, said Mr. Samuelsson.

You have to be very careful when you introduce this, and that’s why I think it has to be safer than perceived,” he said, adding that responsibility for the vehicles “comes back to the ones who are selling the system”. He added: “Doing it without being absolutely convinced the car can handle that [situation] safely, then I think it’s irresponsible.”

Financial Times, March 24, 2019

Over the past week reports surfaced that hackers were able to take over a Model S via remote access and cause it to steer into other lanes without the driver's permission.

So we were perhaps less than enchanted when Musk tweeted after the market closed on Wednesday about what he was most interested in at that moment:

Nothing against the Malabar giant squirrel, which is amazing, but we already had endured Musk's rap song to a gorilla and his infatuation with Dogecoin.

Then we waited another four hours during which time Musk solved a "black screen" issue for Sheryl Crow before Tesla got around to releasing the report Wednesday night.

Finally, the main event.

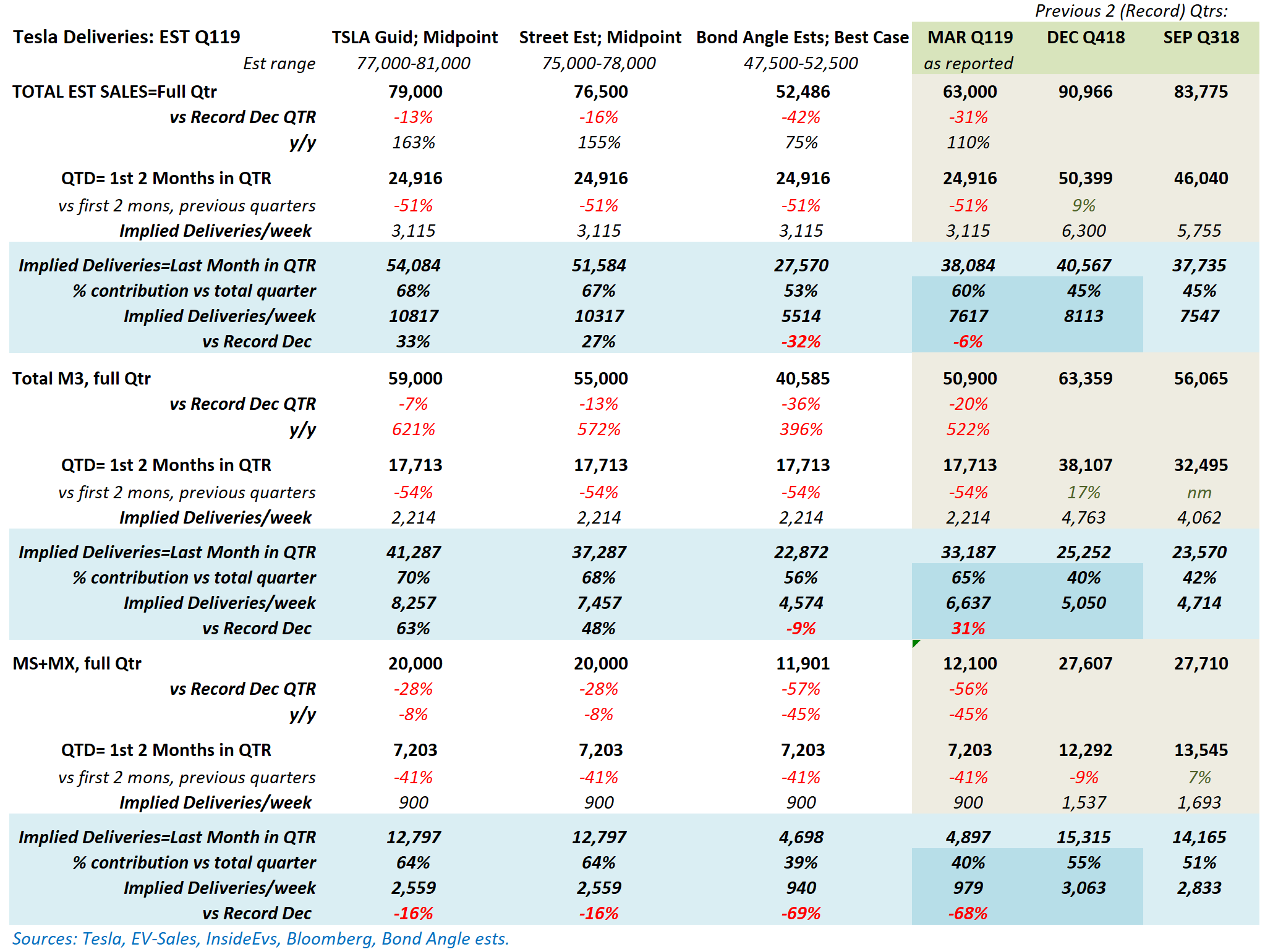

Tesla delivered 63,000 cars for the quarter, up 110% y/y but down 31% versus the record fourth quarter. This comprised roughly 50,900 Model 3s versus 8,182 last year (when Tesla was struggling to ramp-up its new model) but down 20% versus the fourth quarter. Models S and X came in at just 12,100 down 45% y/y; down 56% versus the fourth quarter. Tesla reported 10,600 cars as in transit, but didn't break that out by model.

These results topped my estimate of 52,500 deliveries on better Model 3 sales, thanks to the late surge in overseas deliveries which apparently were more than double US sales according to preliminary estimates by InsideEVs. However, sales of Models S and X plunged as I expected right off the cliff--most likely cannibalized by the launch of Model 3 in Europe and China.

This was well short of what Tesla and market consensus estimates projected, as shown by this updated chart from my last report:

It's obvious that Tesla's sales were foundering in the first two months of the quarter with Model 3 deliveries averaging just 2,200 per week--less than half the pace versus December--and Models S and X sinking to just 900 per week versus 1500-1600 per week the previous quarters. It's also clear the March surge involved only Model 3--Models S and X were little changed.

We can also surmise that the in-transit cars reported at 10,600 were likely Model 3s, and this represents just over two weeks of deliveries. This hardly indicates a "large number of vehicle deliveries" forced to "shift to the second quarter," as Tesla explained. Indeed, Tesla had more cars in transit in the September and December quarters when demand was clearly growing.

Now consider that Tesla's Model 3 production at 62,950 was just 4,840 per week--still trailing the 5,000 per week promised since the June quarter last year. This was little changed versus the fourth quarter and also short of average market estimates for 64,400. The Bloomberg Model 3 Production Tracker had projected more than 79,000 Model 3s produced for the quarter--6,087 per week--which is more than the 77,100 Tesla produced for all three models combined.

Nevertheless, even with the late surge in deliveries overseas and assuming the in-transit cars were Model 3s, Model 3 excess inventory extended to 2.4 weeks versus 1.4 weeks in the fourth quarter and 0.4 weeks in the third quarter.

There are more red flags with Models S and X, where production was slashed by 43% y/y and sequentially and still generated substantial excess inventory. While Model's S & X had indicated 4-6 weeks of available inventory every quarter for more than a year, plunging sales in the quarter to just 930/week versus more than 2100/week the previous two quarters drove excess inventory to nearly 15 weeks.

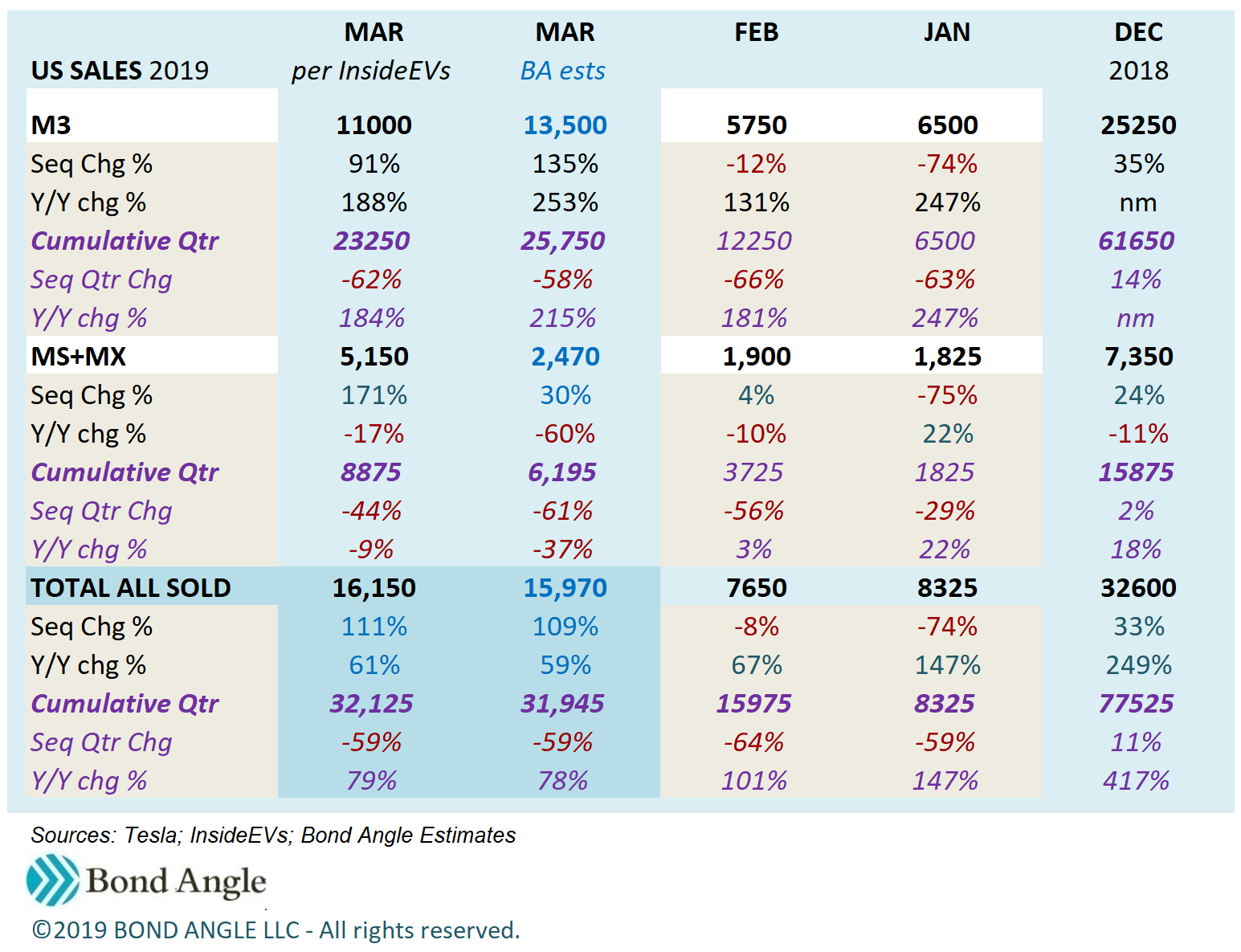

Monthly trends highlight Tesla's continuing sales volatility overall:

But it's also clear that Tesla's US sales are stalling and sales of Models S and X are deeply troubled in the US and abroad:

Tesla admitted that demand was pulled forward into the fourth quarter as customers rushed to buy before emissions credits were reduced. However, early indications suggest Model 3's demand overseas may not continue at the pace seen with its launch this quarter into Europe and China--possibly impaired by the same quality and reliability troubles that already have tempered its appeal in the US.

Indeed, it's not clear where sustainable demand falls for Model 3 or that sales for Models S and X can be meaningfully revived--anywhere.

That's a problem given Tesla's ambitious guidance for deliveries, which it affirmed at 360,000-400,000 for the year. After this troubled quarter, deliveries must average 99,000-112,300 per quarter for the next three quarters to hit Tesla's targets.

But unless we see convincing strength in the second quarter, with Model 3 carrying most of the full load, I now suspect Tesla may have trouble hitting my previous estimate of 340,000 per year which implies an average of 92,400 per quarter the next three quarters.

In the meantime, lower average pricing and likely higher cost pressure from pervasive inefficiency will continue to suppress revenue quality, operating margins, and profits. That also will increase cash consumption and threaten already strained liquidity. First quarter auto segment revenue is now indicated at $4.1 billion (up 60% y/y; down 32% sequentially) and consolidated revenue at $5.3 billion (up 56% y/y; down 26% sequentially), with $565 million in EBITDA (10.7% margin), a net loss of $110 million versus $91 million net income in the fourth quarter and the $710 million loss last year, and $120-300 million in cash consumed in operations.

Maintain “Underperform” on TSLA 5.3% Senior Notes due 2025, up a point since last week at 87.4 (7.8% ytw; 555 bps). That’s just 104 bps of spread per turn of estimated leverage in 2019 on potentially increased borrowing to offset cash shortfalls—hardly adequate compensation for such a volatile issuer with such precarious prospects. Given Tesla's persistent uncertainty and escalating risks, we could see 3-5 points additional downside from here.

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.