Tesla China Sales Deflated in July

Local deliveries in China plunged to the lowest since April 2020. Europe looks little better, as I expected. This may be the start of what turns out to be a much softer Q3 than the market expects.

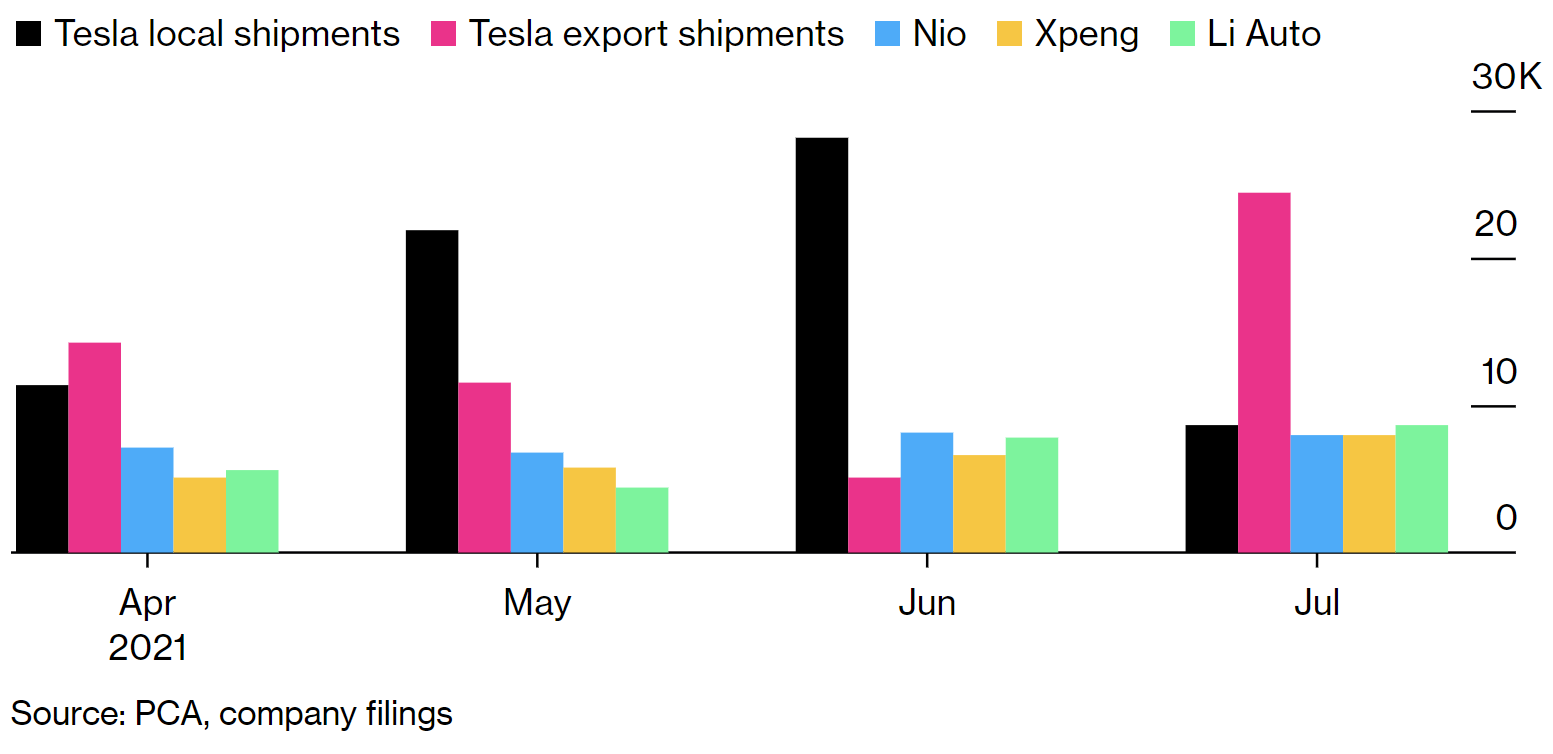

Tesla (TSLA) monthly deliveries in China fell in July to 8,621, down 69% versus June and down 35% versus last year.

But some observers preferred to highlight instead the gross reported number of 32,968, which was down just 1% versus June. But this includes a record 24,357 in exports—not sales—shipped to other markets where they also didn’t sell.

We know this because most of those exports went to Europe, the next largest market after China, where Tesla’s July sales are tracking below 800—a drop of at least 23% versus last year. The rest went to much smaller markets: Japan, Australia, New Zealand, Singapore and Hong Kong, implying something like 23,000 cars sitting in parking lots as unsold inventory.

Tesla fans typically wave off weak sales in the first month of the quarter, but Tesla’s competitors didn’t. Indeed, July sales of EVs jumped 169.4% in China—led by local rivals like giant BYD Company (BYDDF) which sold 24,996, up 109%.

Local EV startups nearly caught Tesla in July, with Nio (NYSE:NIO), XPeng (NYSE:XPEV) and Li Auto (NASDAQ:LI) each selling roughly 8,000 or better.

Tesla’s MIC Model 3 sales, by comparison, were a tepid 6,601, down 60% versus June and down 43% y/y. That wasn’t the worst news.

MIC Model Y tumbled to just 2,397, down 79% versus June and the lowest since it launched in January with 1,970.

This may be at least partially due to buyers waiting for the cheaper RWD Standard Range Model Y, which became available the first week of July. Of course, this also was the given excuse when Model Y sales fell 9% in June, less than six months after launch.

Model Y RWD SR costs about 20% less at 276,000 yuan ($42,600) after government subsidies compared with the longer range version. Its range is sharply lower at roughly 240 miles, which is why CEO Elon Musk cancelled the very same model in the US last year.

So there’s a good chance this model also may have trouble catching on in China given plenty of strong local competition with similar to higher range and lower prices. If so, it won’t solve Tesla’s problems with sagging Model Y sales already.

This could be why Tesla ended up exporting 8,210 Model Ys it couldn’t sell in China in July.

Let’s not forget that Elon Musk had boasted Tesla would need several plants just to meet demand in China. In reality, Tesla had to export 3x as many cars than it was able to sell in China to much smaller markets.

With disappointing numbers as indicated so far from China and Europe, which potentially contributed 35-40% of total deliveries, total deliveries for the month may be 24,000-27,000 (down 18-29% y/y). If so, this means Tesla needs a record 174,000-178,000 deliveries for the next two months just to equal deliveries in the June quarter.

If that doesn’t happen, July was a particularly weak start to what may become a softer than expected quarter, especially compared with sharply higher market expectations.

I had projected Q3 deliveries flat to slightly higher versus Q2 and Q4 deliveries up roughly 5-10% versus Q3. This implied roughly 800,000-822,000 for the year, well below market consensus (see my model and projections in Tesla’s Car Business Finally Turned A Profit. Really. Time For A Big Bond Deal on 8/5/21).

So far, trends continue to align with my concerns as far back as February for a more challenging second half of the year, including my warnings about stalling Model Y. My doubts that Cybertruck and Semi-Truck would launch this year were just confirmed by Tesla.

I continue to assume erosion in the US and Europe for Models 3, S, & X, with primary growth from Model Y in the US, Europe, and China, and stalling MIC Model 3 as MIC Model Y takes hold. There’s an increasing chance Model Y sales fade faster than the market expects in the second half of the year, similar to trends I have tracked with Model 3. I assume only modest sales at best from Cybertruck and Semi-Truck launches later in the year, if at all.

Tesla Is Falling and It Can't Get Up, 2/27/21

We’ll see.

Tesla's 5.3% senior notes due 2025 are lower since my last report and now trading near the call price at 102.6 (2.5% ytw; 165 bps). This offers no upside given that these bonds are being called as I projected (see Tesla Goes To Record Extremes To Create Q1 "Profits" on 4/28/21). I still suspect Tesla may issue new bonds to refinance this issue, possibly sweetened by a credit quality upgrade to at or near investment grade and yield near 2%. Maintain "Underperform."

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.