Tesla Q1 Trends: Rockslide

You know it's bad when delivery trends blow through even my lowest estimates—no thanks to the hapless CyberTruck which continues to shoot Tesla in the foot.

Tesla’s (TSLA 0.00%↑) first quarter is going seriously wrong. Second-quarter deliveries in February looked far worse y/y and sequentially versus the same period in the previous quarter, even compared with disturbingly weak January results—confirming again my concern that growth momentum has stalled (see Tesla: Moving The Goalposts Works Until It Doesn't, 1/26/24).

Results were particularly weak in China and Europe, the world’s largest EV markets, where Tesla had generated 54.3% of tepid Q4 results.

Two-month deliveries in Europe, which contributed 19.2% (down 400 bps) of Q4 results, are down 11% y/y and down 16% versus the first two months of Q4—breaking a nearly 2-year trend of continuous growth at this point in the quarter. Deliveries turned solidly red for the quarter on the 19% y/y drop in February which was due primarily to the 42% y/y decline in Model 3 to just 6,960 (25% of the monthly total) and the 5% y/y decline in Model Y to just 20,457 (74% of the monthly total).

China deliveries also plunged in February, down 11% y/y to 30,141, with Model 3 down 9% to 7,604 and Model Y down 12% to 22,537 (source: China Passenger Car Association (CPCA)). This offset stronger January sales of 39,881 (up a slowing but still solid 49% y/y) when still growing Model Y sales (up 111% to 29.912) managed to cover the 21% drop in Model 3 to 9,969. Two-month deliveries were up just 15% y/y to 70,022—the weakest in five quarters and the slowest growth in nearly two years.

Given the record pile-up in already bloated inventories in every key market, especially the flagship Model Y in the US, March trends are even more disturbing—as tracked by TeslaInfo.com:

Modest Cybertruck sales haven’t moved the needle, as I expected, nor are they likely to in the foreseeable future. Indeed, the long-delayed addition to Tesla’s small and aging fleet may be getting as much attention for its failures as for its quirky looks given how much has been written about its poor build quality (par for Tesla, as I’ve long noted) plus dramatic mechanical failures which have already have left a striking number of the few hundred initial buyers stranded with dead trucks. No wonder reports are circulating about spiking order cancellations. Since Tesla can’t afford to make Cybertruck profitable even at the whopping $100k price tag, this may save it money.

The bottom line is that total Q1 sales seem much weaker than even my below-market estimates which called for deliveries flat to down 3% versus disappointing Q4 results (see Elon Musk Can't Be Trusted. He Also Can't Be Stopped, Apparently, 2/28/24).

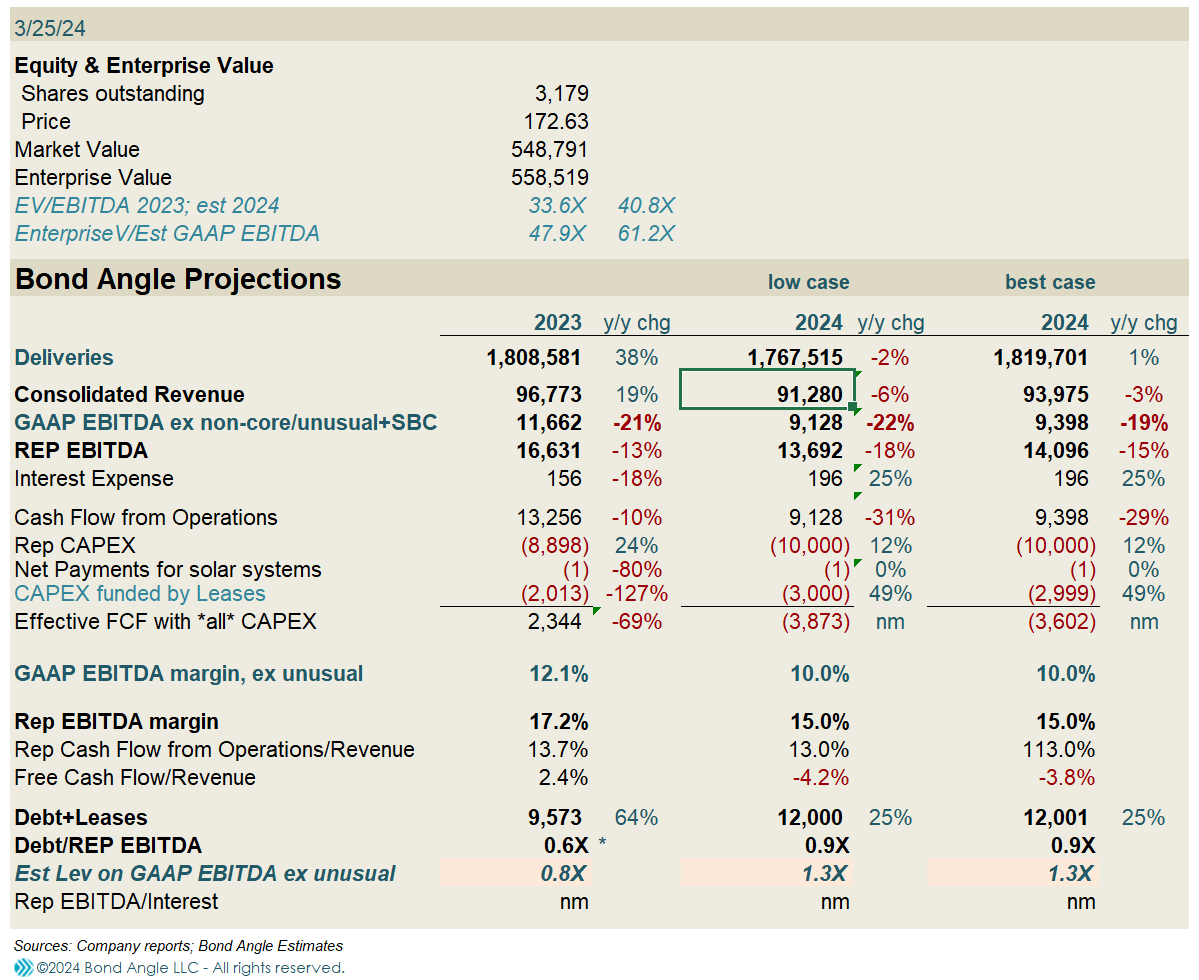

Now it looks to me like Q1 deliveries could be flat to down 3% to 411,000-424,000 versus weaker than expected Q1 results last year (see Tesla Q1 Deliveries "Beat" Rapidly Falling Market Estimates But Miss Management Guidance, 4/3/23).

This indicates Q1 revenue at $21.6-22.2 billion (down 5-8% y/y), with EBITDA at $3.1-3.2 billion (14.5% margin; down 380 bps) and net income at $1.7-1.8 billion (down 29-31% y/y).

For the full year, I now estimate deliveries at 1.77 billion (down 2% y/y) to 1.82 billion (up 1% y/y). This indicates 2024 revenue at $91.3-94 billion (down 3-6% y/y), with EBITDA at $13.7-14.1 billion (down 15-18%) and net income at $9.1-9.5 billion (down 37-39% y/y).

Stay tuned.

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.