Tesla Q2 Deliveries Beat; Demand and Profit Trends Less Clear

Deliveries surged; see why it may not be enough.

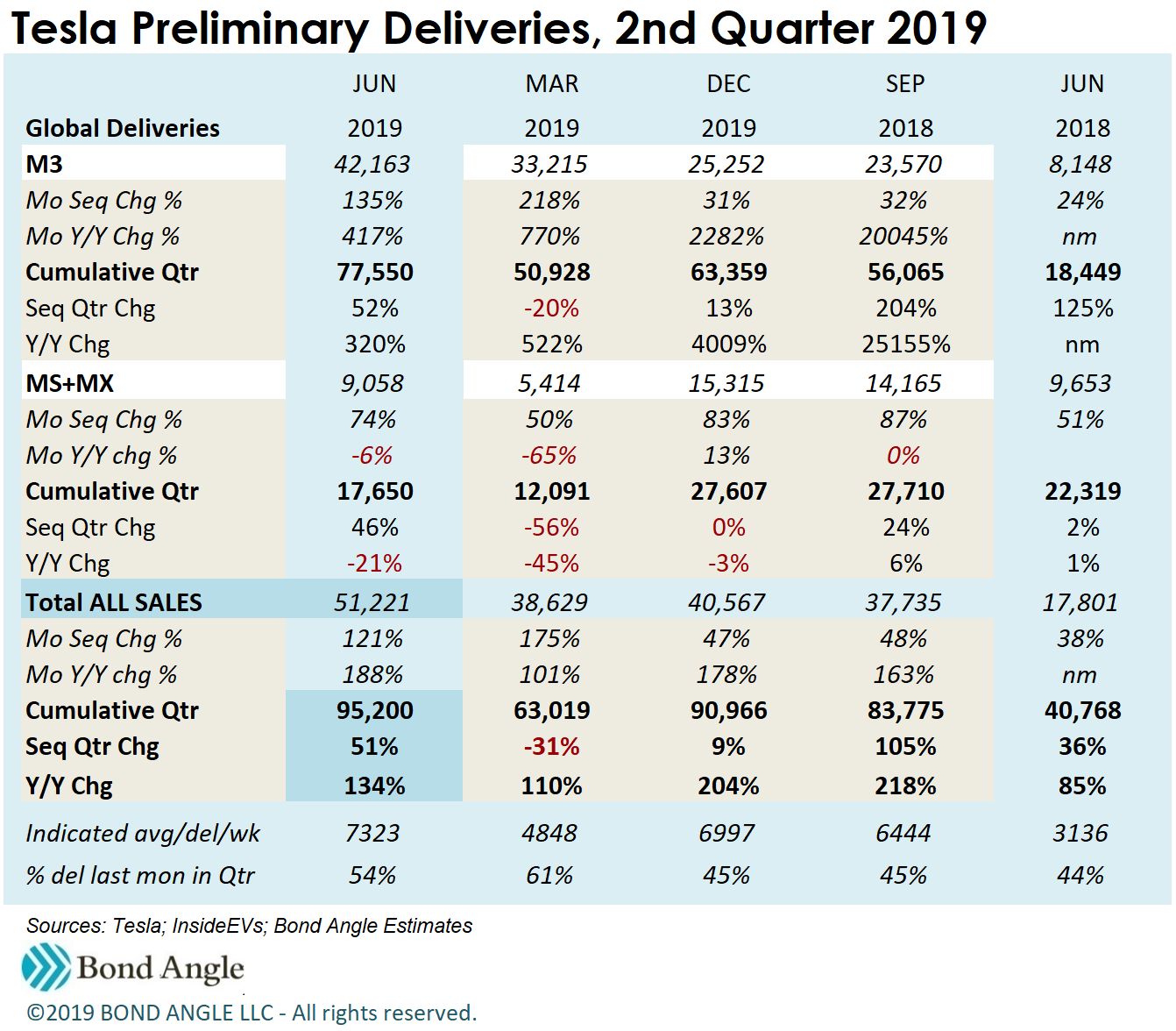

Tesla (TSLA)reported a record 95,200 deliveries for the second quarter in its preliminary report out last Tuesday, topping reduced market estimates.

Year-to-date results surged to 158,219, but this still was far short of 180,000-200,000 where Tesla should be averaging on its way to its projected 360,000-400,000 for the year.

Also interesting, as I commented Tuesday, was that Tesla did not affirm guidance for the year as it had done even after reporting disastrous first quarter results last April which had tracked well below the company's forecast as well as market expectations. Tesla then had notably assured investors that cash on hand remained "sufficient" even as it admitted the stunning drop in deliveries plus severe price cuts had "negatively impacted" first-quarter net income.

Those proved to be glaring understatements. Tesla reported ajarring first-quarter loss of $702 million and cash at less than $2.2 billion--down 40% versus the fourth quarter and the lowest since March 2016.

So it's troubling that Tesla generated record deliveries in the second quarter and yet didn't see fit to update its expectations for annual deliveries or its forecast to generate positive free cash flow and "significantly reduce our loss in Q2."

Considering Tesla typically is happy to crow when it has good news to report, this doesn't bode well for full second-quarter results which the company is expected to report in late July or early August.

What if you had a late surge and nobody came?

Tesla had projected 90,000-100,000 deliveries for the quarter, but investors were wary about falling for that again.

CEO Elon Musk even signaled record results in two emails to employees conveniently leaked in late May, but this failed to revive Tesla's stock which slumped to a two year low of $179 by June 3rd--down 46% for the year and well below $243 where Tesla had priced its secondary offering May 3rd. Tesla's benchmark 5.3% senior notes hit an all-time low at 81.3 on May 29th. By the end of the quarter, market expectations for deliveries, revenue, and profit for the quarter had been dramatically reduced.

But this time Tesla's guidance for deliveries proved accurate. Whether it was settling conditions following the sales strategy chaos evident in the first quarter, or continuing aggressive price discounts and incentives, or the threat of further cuts in emissions credits starting July 1st, or some combination of all these factors, deliveries were convincingly improved versus the disappointing first quarter.

Model 3 deliveries clocked in at a record 77,500, up 52% versus the first quarter and up 320% versus last year when the M3 ramp-up was just beginning to take hold. Models S and X rebounded to 17,650, up 46% versus the first quarter but still down 21% versus last year.

This was enough to extend the rebound in Tesla stock and bonds which had been spurred ahead of the company's shareholder's meeting in mid-June. The stock closed last Friday at $233 and the 5.3% notes rose to 89.5 (7.5% ytw), almost back to the 89.7 high for the year hit back in February.

This was an impressive rebound, particularly for the bonds, though it most likely was also helped by the recent surge of yield-chasing fund flows into the high yield market.

In any case, such enthusiasm for Tesla bonds seems premature since the company apparently wasn't confident enough to comment as it has in the past about existing delivery guidance for the year, much less about revenue and potential losses for the quarter which could threaten further its already tenuous financial condition.

Signs of trouble at home and abroad

Demand for all models remained in flux, with more than half of deliveries reported for the quarter again coming in the last month. Check out the chart below which shows sequential and y/y comparisons for the last five quarters as well as the last month in each quarter.

At first glance, we can see persisting weakness in sales of pricey, higher margin Models S and X which continued to decline y/y--they are down by double-digit percentages for now six straight months. This dramatic change in mix versus the less profitable M3 plus price discounting across all models will have a severe impact on operating margins in the second quarter and beyond.

One can also see that Tesla closed the last two quarters with a mad sales rush in the last month, and across all models, which apparently was still necessary after said price discounts and other expensive incentives.

According to Tesla, this wasn't supposed to happen. When pledging back in April to deliver 90,000-100,000 cars in the second quarter, the company said it planned to better balance deliveries more uniformly throughout the quarter:

"Although it is possible to deliver a higher number of vehicles, we believe it is important to begin unwinding the "wave" approach to vehicle deliveries, where overseas cars have been made in the first half of the quarter and North American cars have been made in the second half. This puts extreme stress on Tesla, negatively affects our working capital needs and adds to our cost structure."

However, a quick scan in the chart of MS+MX deliveries, which have not been affected by new production ramp-ups or market expansions, shows that same last month sales surge in three of the past five quarters--historical trends mark five of the past eight quarters. It's an entrenched pattern.

This quarter was expected to be stronger versus the first quarter, but also more stable

Another perhaps more compelling reason deliveries in the second quarter should have been significantly more balanced versus the first quarter is that the expansion of M3 into Europe and China started back in February and should have been, according to Tesla, well underway by the June quarter.

Tesla also said it concentrated on production for Europe and China in the first half of the first quarter, so US deliveries were concentrated in the last half of the month. Indeed, we know Tesla delivered more than 30,000 vehicles the last ten days of March--more than half the total delivered for the entire quarter.

Monthly sales trends look even more problematic

The chart below shows deliveries at just 43,979 through the end of May. That's just 44-49% of the total 90,000-100,000 deliveries projected by management for the quarter. And as I have observed, Tesla really needed to average 99,000-112,000 in each of the next three quarters to meet guidance for the year.

April didn't help much. There were 10,600 cars, likely M3s, identified as in transit but not yet delivered to customers at the end of March to count as US deliveries--perfect for a strong start to the second quarter. Good thing, since demand seemed to dry up in April as it appears those cars in transit may have comprised most all cars delivered for the month in the US versus 7,372 delivered overseas--and more than half the cars delivered for the month overall.

Indeed, those cars in-transit turned out to contribute 14% to total M3 deliveries for the quarter. In-transit cars have contributed from 10-30% or more of the subsequent quarter's deliveries over the past few years, making them a valuable indicator of core sales and forward demand strength. Indeed, this quarter the number dropped to just 7,400.

So it's troubling that Tesla has decided not to report cars in transit going forward.

May was even more disappointing for M3 overseas, with deliveries indicated down 46% to just 4,015. Sales in Europe and Canada were encouraging, though it's also possible that Tesla may have gamed the emissions credit program to boost Canadian sales--pulling demand forward.

China was significantly weaker, potentially a consequence of Tesla's hefty price discounting there which alienated prospective buyers who decided just to wait for more price cuts later, if at all. I suspect these trends continued into June when deliveries rebounded to 20,938 but still were down 9% versus March when shipment volumes first started arriving in size.

Home is where the hurt is

While M3 demand is sorting out overseas just as serious competition also takes hold, it now has been for sale at scale in the US for more than a year.

And in the US, home sweet home, it appears the days of "insane demand" for M3 are over.

In the chart below, I broke out US sales by month, for every month back to and including June last year when M3 was formally rolled out in size.

Notice that every month in each quarter this year, comparing months 1, months 2, and months 3 of each quarter accordingly, trail versus the comparable months in the third and fourth quarters last year.

So, in the record quarter for overall deliveries Tesla just announced, M3 deliveries in the US have trailed every month this year versus the comparable months in the third and fourth quarters last year when M3 was as hot as it's ever going to get.

This, I suspect, may better explain why Tesla might be concerned with meeting its previous 360,000-400,000 deliveries guidance for the year, much less the now 100,900-120,900 per quarter deliveries it will need to average in the remaining two quarters.

Now consider Tesla has been pedaling really, really hard and straight uphill to churn out the June quarter. The cost was dear. Multiple rounds of substantial price cuts starting in the third quarter last year plus additional offerings of options and deal discounts have failed to boost sales to last year's torrid pace. But they have shrunk margins faster and deeper than Tesla's severe cost-cutting measures can absorb.

This indicates revenue and profit plus free cash flow and cash on hand much lower by comparison versus what Tesla could generate on similar deliveries in the last half of last year.

As a result, my adjusted estimates are only modestly improved versus my cautious projections in May. Auto sales revenue is now indicated at $5.4 billion, including emissions credits, which is up 72% y/y but down 9% versus the record December fourth quarter. This pegs consolidated revenue at $6.3 billion (up 58% y/y; down 13% versus the fourth quarter), with EBITDA near $300 million (4.7% margin) and a net loss of $250-450 million. Free cash flow after reduced capex is indicated to be nominal at best; from breakeven to $130 million--less than the $165 million Tesla still owes on its long overdue SolarCity term loan. Leverage could increase to 5.9x or more on substantial debt borrowed during the quarter plus $50 million in new debt added with the Maxwell Technologies acquisition (and count on Tesla coveting even Maxwell's modest $48 million in cash).

This outlook does little to substantially ease Tesla's liquidity trouble, as I noted back in May:

The $1.54 billion net proceeds from the bond sale fall just short of covering the working capital deficit of $1.56 billion at the end of the [first] quarter, which included $3.25 billion in accounts payable and $2.28 billion in accrued current liabilities. The $848 million netted from the stock sale barely covers remaining debt due the rest of the year ($165 million for the delayed term loan plus $566 million in convertible bonds maturing in November).

This leaves indicated effective available cash little improved versus my $613 million estimate as of June 30th [before borrowing], and far short of $1.72 billion projected in capex for the rest of the year plus another $700-800 million in interest payments.

So it looks like Tesla may need an additional $2 billion in cash, at least, to maintain effective available cash on hand at minimally sustainable levels, preferably generated as free cash flow from core operations versus sources from noncore and unusual items plus additional borrowing as it has done virtually every quarter for years.

Revenue and profit trends may be little improved if, as I suspect, Tesla's quarterly delivery trends average at less than 95,000-100,000 per quarter for the next few quarters—I estimate 348,000-358,000 for 2019.

If so, this would help confirm, as I speculated in May, why Tesla elected to sell stock and bonds when market prices were near record lows rather than wait a mere month or so to report what should be record revenue and profits to go with record deliveries (see "Tesla: When a Spartan Diet + $2 Billion Isn’t Enough").

Instead, Tesla apparently doesn't expect to generate sustainable profits from operations sufficient to ease its chronic liquidity pressure and meet its sizable and escalating near-term cash obligations.

Maintain “Underperform” on TSLA 5.3% Senior Notes due 2025, which have rallied 5 points since my last report to 89.5 (7.5% ytw; 570 bps). That’s a measly 95 bps of spread per turn of estimated leverage in 2019, woefully inadequate compensation for such a volatile issuer with such precarious prospects. Given Tesla's persistent uncertainty and escalating risks, we could see 5 or more points of downside from here.

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.