The Tide Is Out and WeWork Bondholders Are Naked

To WeWork bondholders: the party's over, the beach is empty, and no one is available to take your call.

To WeWork bondholders: The party's over, the beach is empty, and no one is available to take your call.

The folks who bought into and/or sold The We Company (WeWork) (WE US) as worth $50 billion, $60 billion, $100 billion--including its largest investors like Softbank Group (9984 JP), its banks, and its new joint-CEOs--are cloistered in intensely uncomfortable CYA meetings now that WeWork's equity value may be worth closer to $3 billion (less than 1x 2019 revenue) by my estimate.

Chastened Fitch and Standard & Poor's belatedly dropped the company's credit ratings last week to deep junk quality with a "negative" outlook. Even WeWork's legacy bankers who pitched its highest equity valuations last year still refuse to close any part of pending loans for the company they arranged in August.

The only investors piling into WeWork debt are short-sellerswho have taken on more than 10% of the company's smallish (read: already hard to trade) $669 million in bonds outstanding which now yield a stunning 12%, hoping to buy back on the cheap as prices drop even more.

They likely will fall.WeWork's failed IPO evaporated billions in equity market value as well as lucrative business opportunities and seemingly endless cash and available credit formerly available, based on its inflated worth, as it marched around the globe doing deals potentially now in trouble.

WeWork bondholders are stuck with the shell that's left, and that's not the worst news.

No One Loves WeWork Anymore, Especially Not its Banks

Not only has WeWork been substantially overvalued for years, as I noted in Gravity Works As WeWork Doesn’t; Now Plan B, it’s legacy banks JPMorgan Chase & Co (JPM US) and Goldman Sachs Group (GS US) helped make that happen as early and recurring investors and lenders.

These same banks along with Morgan Stanley (MS US) pitched WeWork to investors at values as high as $104 billion in 2018, and fought over leading the IPO offering. Yet by August of this year, as they also arranged $6 billion in new credit facilities set to close concurrently with the estimated $3-4 billion IPO, I noted clear signals they were spooked.

As I detailed in Gravity Works As WeWork Doesn’t; Now Plan B, the banks planned to charge substantially higher interest and fees on the new credit facilities, with potentially more restrictive covenants as well, versus its existing facility, and were willing to loan for only three years versus the previous five-year term.

These were tentative agreements marked as of August 13 that likely fell into jeopardy as market scrutiny of WeWork's S-1 filed the next day began to demolish expectations for the IPO.

The IPO was in trouble right out of the gate as investor enthusiasm gave way to skepticism, heated criticism, and then outright alarm over WeWork's irritatingly oblique and thoroughly insufficient disclosure, the company's dubious operating metrics, and a surprisingly more precarious than advertised financial condition which challenged its ambitious claims and forecasts--and especially it's extravagant $47 billion equity market value floated since in January.

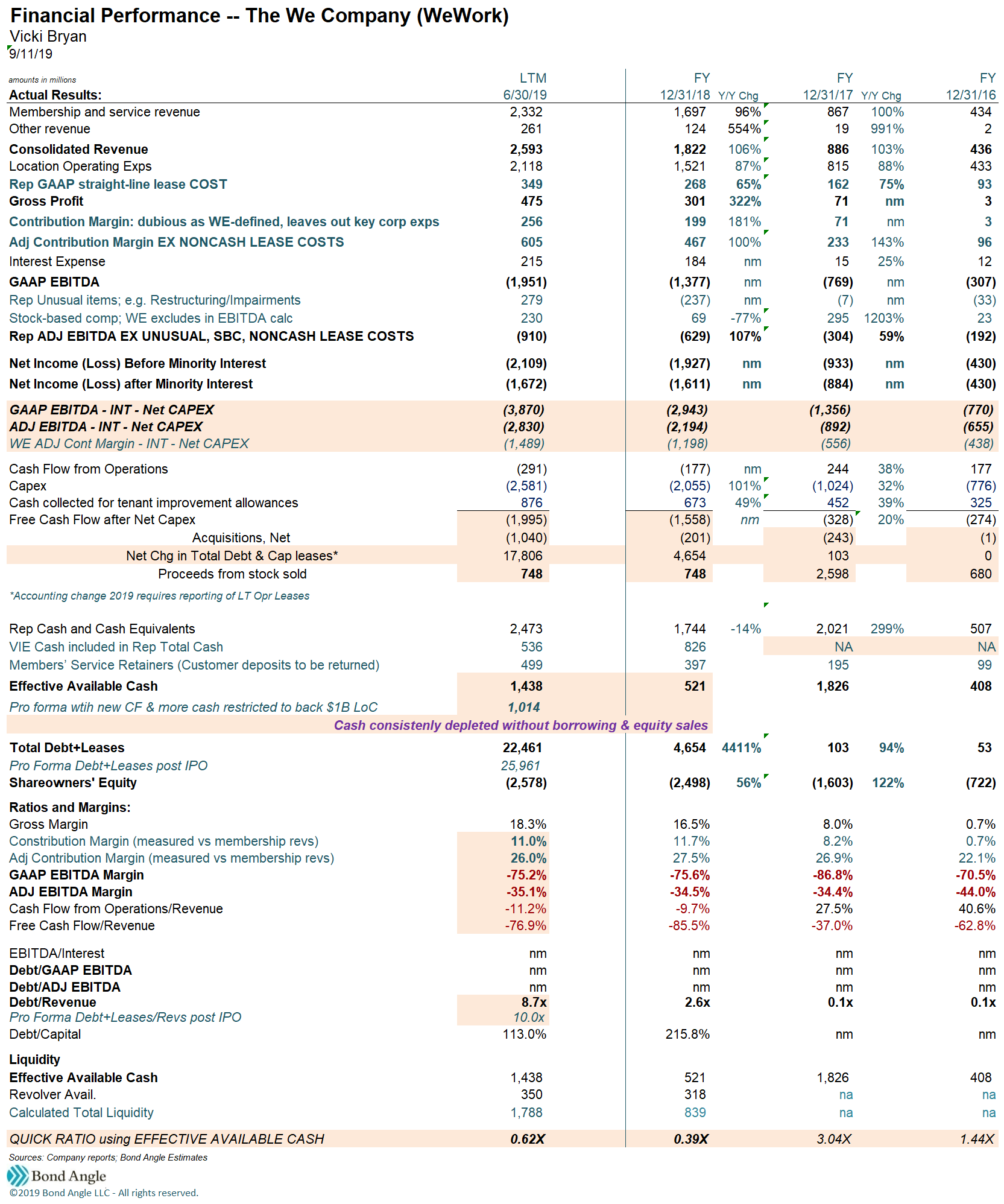

My work has shown WeWork's profitability substantially lower versus reported and eroding rapidly, with likely years of losses and severe cash consumption still ahead.

Cash burn has been the most alarming, with WeWork effectively consuming $5.5 billion in 2018--3x revenue generated and all funded from borrowing and equity infusions, as has happened every year of its nine-year history.

At this pace, WeWork was set to consume all the $9-10 billion it planned to raise in stock and debt in a year or less, with still no convincing path to profits or positive free cash flow. And then what?

As it stands, the $1.4 billion I calculated in effectively available cash on hand as of June 30th, $1 billion less versus reported, may be depleted by yearend.

WeWork's banks had to have known all this long before the IPO was announced, certainly before the S-1 was filed--now they can't move forward? It's been three weeks since the IPO collapsed, and nearly two months since mid-August when it was clear to me the banks were concerned. That's how long WeWork likely has been trying to negotiate with its increasingly worried banks.

Without ample new credit, WeWork will struggle mightily to stay afloat long enough to fund its recovery--much less initiate and comfortably service new business deals. This includes debt-funded transactions closed subsequent to the S-1 filing in August according to CMBS specialist Trepp, which recently warned again about "meaningful" exposure to WeWork leases in $3.3 billion of CMBS debt in an interview on a recent Debtwire podcast, "ABS in Mind: WeWork, the unwanted tenant."

As I always say, banks get much more timely and comprehensive financial information than public investors, and so are in the best position to know what's really going on under WeWork's hood and beyond. Now they don't like what they see:

WeWork's prospects have been shredded. Just weeks ago WeWork still was being celebrated as the largest and fastest-growing tenant for commercial office space in some of the most important cities worldwide, including New York City, Chicago, Dublin, and London, aiming for an astonishing $3 trillion in global revenue opportunities as of its S-1 filing.

Now WeWork has become a bright red flag in those markets with current and prospective customers and landlords scrambling to assess its viability going forward. WeWork's new joint-CEOs, as their first order of business last week, terminated current negotiations with landlords for new lease agreements and sharply curtailed others to preserve cash. New business WeWork was expected to get is being snapped up by rivals, which also are taking calls from WeWork landlords about potentially taking over if the company fails. Other deals have fallen apart because counterparties are wary about signing up business WeWork potentially can't afford to execute.

WeWork can't quickly or easily slash its most expensive cost: rent. WeWork has a stunning $47 billion in long-term lease obligations, signed in many of the most expensive markets in the world. Its commitments are so large that signing those agreements influenced commercial building and rent prices going up just as they will as WeWork tries now to renegotiate terms--good luck with that. I estimate WeWork could spend $2.5 billion in rent expense for 2019. That's 76% of potentially $3.3 billion in revenue for the year, before revenue is reduced by sales of subsidiaries and/or eroding sales from spooked customers who opt out of WeWork's short-term contracts. WeWork already lost $2.1 billion on $2.6 billion in trailing 12-month revenue as of June 30th. I estimate its tracking a net loss near $3 billion for the year.

WeWork's precarious ability to service its leases also complicates its bank negotiations, since it backs its leases with "letters of credit, cash security deposits and surety bonds." If WeWork defaults on its leases:

The applicable landlords could draw under the letters of credit or demand payment under the surety bonds, which could adversely affect our financial condition and liquidity. In addition, under our surety bonds, the applicable surety has the right to request collateral, including cash collateral or letters of credit, at any time the surety bonds are outstanding. We are also pursuing strategic alternatives to pure leasing arrangements, including management agreements, participating leases and other occupancy arrangements with respect to spaces. Some of our agreements contain penalties that are payable in the event we terminate the arrangement. In addition, we have limited experience to date with these types of transactions, and we may not be able to successfully complete additional transactions on commercially reasonable terms or at all."

WeWork S-1

WeWork's escalating business pressures have spiked risks that it may default on its leases, which also threatens cash and asset value WeWork's banks require to secure the company's current as well as proposed credit facilities.

WeWork's frantic efforts to slash its other operating costs and to sell assets to preserve cash won't be enough to restore financial stability any time soon. The company is laying off 25% of its workforce, so far, but what's needed it a complete shakeup of its cost structure.

I have projected worsening trends through next year, but let's just look at WeWork's recent results to make this point. In the latest twelve months as of June 30, WeWork spent $2.1 billion (82%) of nearly $2.6 billion in revenue on direct operating expenses (mostly rent plus labor, utilities, maintenance, etc.), so it's hard to see meaningful reduction here.

It reported another $2.43 billion in expenses on top of that, not including $432 million in depreciation: $1.3 billion in general overhead and other operating expenses plus $1.1 billion in preopening, growth, and "new market" expenses--which accounted for the entire $2.4 billion loss reported in earnings before interest and taxes.

So even in this simplified example, we can see cutting all the $1.1 billion in supposed growth-related expenses still implies negative EBIT by $1.3 billion as even drastically reduced operating costs indicated at $3.9 billion overwhelm $2.6 billion in revenue.

Not surprising then that selling noncore and likely unprofitable assets like Managed by Q, Meetup, Conductor, SpaceIQ, and Teem, all on the chopping block, will barely move the needle in operating margins and may, at best, net only nominal cash versus what WeWork paid for them.

No wonder plans urgently underway to salvage WeWork as a going concern as well as its business prospects haven't been enough so far to convince the banks that it can:

comfortably provide and sustain sufficient collateral to support a now sharply reduced $3 billion credit facility, even with Softbank kicking in another $1 billion in cash from fresh equity in addition to the $1.5 billion it already had pledged to invest in 2020.

manage the increased debt load after new bank loans are quickly drawn, and

generate sufficiently improving operating performance to demonstrate it can service leases and debt as well as capex and other cash obligations over the foreseeable future.

We're actually seeing WeWork play out the scenario it told investors for years wouldn't happen: revenue stalling or falling due to troubled business conditions (its own) while its cost structure remains untenably high versus its massive and growing cash and lease-adjusted debt obligations.

This cliffhanger arrives as the cone of silence comes down on information from WeWork going forward.

Say Goodbye to Publicly Available Information

The only reason we know as much as we do know about WeWork, warts and all, is because WeWork was mandated to provide in the S-1 filing at least the minimum standard of information required by the SEC to protect potential investors. Now WeWork has withdrawn that S-1 as well as its commitment to the information it had provided.

No IPO, no more public filings about financial performance going forward.

Otherwise, WeWork is only required by its bond indenture to provide financial reports to holders or "prospective holders" of its bonds. Reported financial information need only be "essentially" complete to the extent it was provided in the bond prospectus and does not have to be certified by WeWork senior officers as correct and true.

Prospective bond investors should have insisted before the deal closed--as I did many times during my years on the buy-side--that WeWork agree in writing in the indenture to provide management-certified financial other SEC-required reports to all "holders, prospective holders, and security analysts" to ensure broadly disseminated transparency of comprehensive information to benefit investors as well as facilitate accurate market pricing and trading.

It's obvious that providing information only to bondholders before and after the notes were issued in April last year has been woefully inadequate as a reliable measure of the company's financial health or operating prowess, little better versus news reports about exuberant private investors who drove WeWork's equity value to $47 billion or its banks that pitched it as high as $100 billion in pursued of hundreds of millions in fees.

In April 2018, when WeWork issued its bonds, then its first-ever public offering, the company was already one of most highly valued US startups ever at $20 billion mostly on the $4.4 billion equity investment by Softbank the previous August. Skeptics at the time were waved off because demand for the bonds was hot--the deal size was increased to $702 million versus the initial $500 million offered, mostly on the seemingly rich 7.875% yield where they priced at par.

However, the bond prospectus did reveal that WeWork's rapidly growing revenue was being outrun by alarming losses while cash flow remained severely negative and lease obligations had ballooned to a troubling $18 billion. WeWork also used dubious metrics like Community Adjusted EBITDA, which is a manufactured measure renamed as Adjusted Contribution Margin in the IPO S-1 (and which I debunked in Gravity Works As WeWork Doesn’t; Now Plan B) that essentially strips out sales costs and other core expenses to generate positive credit metrics. It's clearly a farce, as my model above shows, since 2017 Community Adjusted EBITDA created an implausible $1 billion boost to the appearance of profitability versus GAAP EBITDA which was -$769 million.

Indeed, the IPO S-1 showed WeWork's profit margins eroding and losses spiking alarmingly during the June 2018 quarter as the bonds were being sold--and in every quarter after that through June 2019. As a result, reported Goldilocks Community Adjusted EBITDA--reported to bondholders only--looked $1.8 billion better versus GAAP EBITDA of -$1.4 billion for 2018 and $2.6 billion better versus GAAP EBITDA at -$2 billion for LTM as of June 30th. This as WeWork burned through $6-8 billion in cash 2018 through June 2019, including all the cash raised from borrowing and equity infusions while lease obligations nearly tripled to $47 billion.

You wouldn't have perceived such marked and escalating risk from the comparatively generous bond credit quality ratings from Standard & Poor's and Fitch, which rated the new bonds "B+" and "BB," respectively, with stable outlooks. These more "middle of the road" high yield credit ratings signal more comfortably stable financial conditions versus WeWork's perpetual red ink chaos.

Only last week did S&P lower its rating a notch to B, only now concerned about WeWork's liquidity pressure and "heightened strategic and governance uncertainty" which may complicate its ability to raise capital--more than a month after the IPO had to be pulled as spectacularly failed. Fitch offered similarly "breaking news" last week that “in the absence of an IPO and associated senior secured debt raise, WeWork does not have sufficient funding to meet its growth plan” when it also dropped its bond rating to "CCC" with a now negative outlook. Ratings now are closer to Moody's original credit rating of "Caa" when the bonds were issued which it withdrew four months later in August 2018 “because it believes it has insufficient or otherwise inadequate information to support maintenance of the ratings.”

That was true. And as a result of such pervasively poor and missing information, WeWork's bonds only traded to record lows, and WeWork's equity only plunged from $50-100 billion valuations to perhaps $3 billion, after the company publicly disclosed comprehensive financial statements with the IPO S-1.

That ship has now sailed.

Contact Us! Unless you want to talk to WeWork Investor Relations:

Now that WeWork has no obligation to provide publicly available information, it really doesn't want to talk to anyone about its bonds. I have tried on several occasions over the past couple of months to contact WeWork Investor Relations during business hours, without success.

Calling the main phone number put me into circuitous phone tag which never connected me to a person, any person, and Investor Relations wasn't even on the menu. I had no luck on the web site under "Contact Us" with "Chat Us", which never responded any time of day on any weekday I tried. Clicking on "Investor Relations" at the bottom of the Contact Us page took me to the gatekeeper box I show above. My submitted request for information as a "securities analyst" has been ignored.

WeWork does, however, offer handy advice on its web site on how others should "speak to "investors," such as "Most investors base their decision largely on the communication they receive from the company itself."

All this means WeWork bondholders find themselves in a more dangerous vacuum than ever. WeWork is likely to remain seriously distressed through next year since it is functionally insolvent, it could run out of cash by yearend, and it can't afford to fund its operations, much less a turnaround via the complete business remodeling it requires.

In the meantime, it's become even more obvious that WeWork does not provide adequate or accurate information to investors and that it likely will remain quiet about serious problems and risks it faces. In the absence of such vital information, market coverage on the bonds will dry up, and so will vital discourse which already resulted in a very healthy and necessary repricing of a WeWork's seriously overvalued equity. This impairs already difficult liquidity in the bonds, leaving bondholders stuck in WeWork's mushroom cave.

WeWork 7.875% senior notes are down 11 points to 83.1 (12.1% ytw/1079 bps) since my last report, and down nearly 20 points since I initiated coverage with a "Sell" rating in Gravity Works As WeWork Doesn’t; Now Plan B when the bonds were at 102.8 (7.3% ytw/540 bps). WeWork remains severely distressed and it's not yet clear whether the company can remain viable for the foreseeable future. Upside potential remains limited as a result given longer-term risks that continue to materialize versus downside risk which could be another 5-10 points from here over the near term. Maintain “Sell.”

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.