WeWork Bonds in Peril As Softbank Abandons Equity Tender

As I projected, Softbank has abandoned its tender offer for $3 billion in WeWork equity, WeWork has no plan B, and WeWork bonds are in freefall.

Softbank Group (9984 JP) has withdrawn its nearly $3 billion tender offer for The We Company (WeWork) (WE US) equity, which I have valued as worthless since last fall.

The news was just reported by Financial Times which confirmed an earlier story by Bloomberg.

I have warned investors for months (most recently in WeWork Prepares Board Fight to Force Softbank to Comply on 3/23/20) that Softbank was struggling even to afford the tender as its own liquidity and financial condition has deteriorated versus its expensive and arguably ill-advised plans which have alarmed its bankers, creditors, bondholders, and investors and thrown its takeover of WeWork into jeopardy.

It now seems increasingly likely that Softbank may walk away from the entire takeover deal any day now—as well it should.

If so, WeWork can do little to shut off multiple bankruptcy alarms from all directions and its bonds are in freefall.

It's Over When It's Over

Softbank signaled this outcome last week when it “told shareholders it had the ability to withdraw from the agreement if it could prove investigations by the Securities and Exchange Commission or the US attorney-general for the Southern District of New York would have a “material adverse effect” on the company, or result in a “material liability” to SoftBank or its Saudi-backed Vision Fund.”

Tonight's news seems to confirm my speculation last week that Softbank is prepared to ignore WeWork's threats of legal action if it abandoned the tender offer as I have expected. Financial Times reported that WeWork's special board committee, advised by the law firm Wilson Sonsini, announced Wednesday night it will “evaluate all of its legal options, including litigation.”

We'll see. I argued last week that Softbank can make a good case that WeWork failed to disclose to existing and prospective investors just how desperate its financial situation really was last fall when it signed the takeover agreement with Softbank after its IPO collapsed. It's a pattern easily demonstrated with years of deliberately misleading management statements and financial reporting from WeWork so problematic that the SEC and The Department of Justice (DoJ) launched investigations that remain ongoing.

Even Softbank's fellow WeWork investors may have trouble denying this in court if they try to join WeWork in suing Softbank to force compliance.

In any case, this outcome presents far less risk to Softbank than proceeding with the tender as I wrote in my last report:

WeWork has little if any bargaining power and can hardly afford an expensive, long-term legal action against Softbank. Whether or not Softbank would lose in court, which is not guaranteed, it seems better served to let WeWork file bankruptcy even though this could mean liquidation.

Softbank might consider writing off the remaining $2 billion or so in WeWork book value as cheaper now versus buying $3 billion in additional worthless equity.

WeWork Prepares Board Fight to Force Softbank to Comply , 3/23/20

We can logically presume friction between Softbank and WeWork has only intensified since they signed the agreement last October—when Softbank had to immediately wire in $1.5 billion to keep WeWork from running out of cash.

I don't doubt that all the key stakeholders involved have been up in arms ever since, including WeWork with Softbank, with its banks, with its other investors, with its top creditors and landlords and customers, and so on. Worse, its already rapid deterioration only escalated during and beyond its dismal fourth quarter that had followed much worse than expected third-quarter results (which tracked my below-market estimates published in Gravity Works As WeWork Doesn't; Now Plan B on 9/17/20).

I imagine Softbank has had similarly intense discussions for months with other WeWork shareholders as well.

There's a good chance most if not all parties involved have remained at odds for months without resolution, even before COVID-19 hit and effectively sealed WeWork's misfortune for the foreseeable future.

Softbank also has struggled increasingly with its wary banks and investors, which also don't agree. Softbank's banks and creditors have been pushing it all year to strengthen its financial condition and curtail its risky financial policies and investments. Its activist shareholders jumped in recently to pressure for the opposite by pushing for massive stock buybacks it can't afford and which will weaken its already strained balance sheet and liquidity. Softbank's futile efforts to please both factions have failed, and it's fallen solidly into junk credit territory as a result with the severe credit quality downgrade by Moody's.

The final straw is that Softbank's significant financial deterioration I warned about for months has now been revealed to the world, damaging its own credibility and prospects (as I discussed in WeWork Prepares Board Fight to Force Softbank to Comply (3/23/20) and in the Smartkarma Webinar | The Softbank WeWork Unwind? (3/18/20).

If WeWork can't recover for years, if at all, and

its equity is likely worthless for the foreseeable future, and

Softbank can't afford additional billions to fund its strugglefor years, and

it's arguably cheaper to let WeWork try to beat it in court (which is far from guaranteed),

Then odds are better than ever that Softbank may now walk away from the entire takeover deal.

Softbank Started to Let Go Months Ago.

I've been tracking how many Softbank-backed troubled companies it recently abandoned to sink or swim. First was Nemaska Lithium, which filed bankruptcy in December (one year after Softbank's nearly $100 million investment for a 10% stake). By then it already was clear to me that WeWork's rescue plan was in trouble (see WeWork Is Foundering While Softbank Struggles With Its Bailout, 11/27/20).

Softbank let two-year-old Brandless file bankruptcy in February, less than two years after Softbank's promised $240 million investment (though only $100 million materialized from Vision Fund). By this point, I had been warning for months that Softbank's tender offer for WeWork equity was in jeopardy (most recently in WeWork's Mounting Losses Send Softbank Scrambling For Alternative Financing on 2/20/20).

Then came last week's bombshell when Oneweb filed bankruptcy, just over three years after Softbank invested $1 billion in it.

Online lender Kabbage abruptly cut off credit lines to its small business clientsover the past week, which may signal its own liquidity pressure. Softbank funded Kabbage two years ago with $250 million.

And these are just some of Softbank's expensive problems with its large stable of struggling, mostly money-losing investments that are not Alibaba Group (BABA US), which is the primary asset backing most of its substantial margin loans.

None of Softbank's losers have been as expensive as WeWork. Indeed WeWork's spectacular collapse has produced stunning losses for Softbank and Vision Fund, and jeopardized the launch of Vision Fund II as prospective investors bolted.

The more than $12 billion Softbank has invested so far in WeWork is a sunk cost long gone. Still, Softbank may be ready to write off the rest of its greatly reduced WeWork book value of $2-3 billion if WeWork files bankruptcy versus investing another $3 billion for worthless equity now, $3.3 billion for new loans to WeWork in coming months, plus $1.75 billion to cover defaults on WeWork's letter of credit facility—potentially as much as $8 billion that WeWork could evaporate just this year.

Without Softbank, WeWork Could Be Done

As I observed last fall, Softbank provided WeWork with a vital boost and hope for the future with the takeover deal just as its credibility was shredded. WeWork probably can't recover without it.

This is no doubt a major obstacle now as WeWork scrambles to get a 30% cut in rents from landlords which hold more than $50 billion in mostly overpriced, long-term leases (on top of obvious other problems I detailed in WeWork Prepares Board Fight to Force Softbank to Comply on 3/23/20).

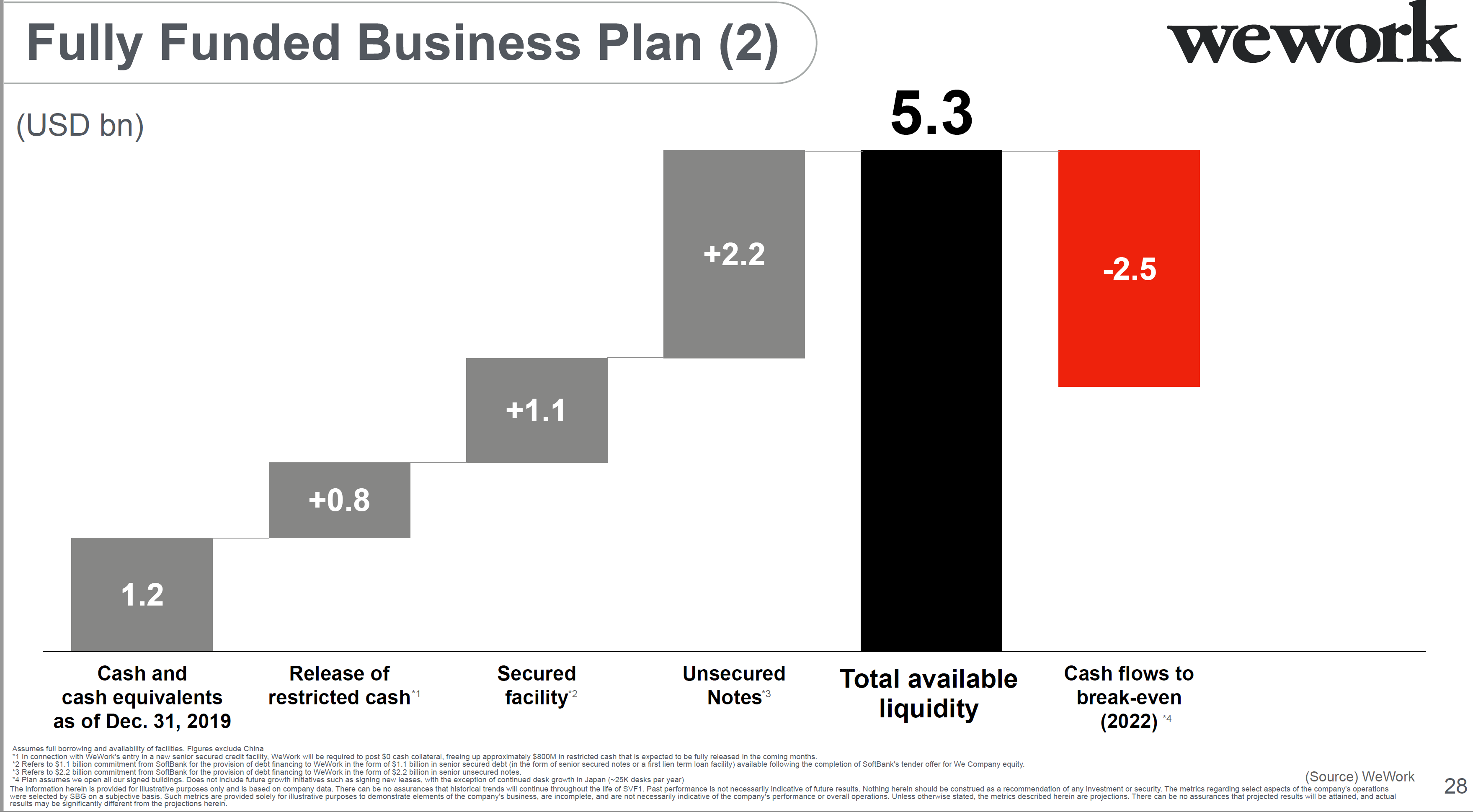

It also explains WeWork's surprising release last week of information about its purportedly strong liquidity position as of December 31st, as shown in this latest slide:

WeWork does not have $4.4 billion in available liquidity, as highlighted in the slide above, much less $5.5 billion advertised as available soon.

As I have noted in previous reports, WeWork reports cash as available it doesn't own and can't actually spend as general operating cash:

Of the $1.3 billion reported as of December 31st, at least $600 million was reportedly owned by subsidiaries (VIEs) as of September 30th, with at least $500 million held as member deposits for leasehold improvements WeWork is obligated to complete (see WeWork's Mounting Losses Send Softbank Scrambling For Alternative Financing on 2/20/20).

Similarly, the $100 million still expected from Softbank "commitments to Japan Co" have been carried as pro forma since before September 30th, apparently may or may not be paid, and are owned by that VIE—not WeWork.

The remaining $100 million of the $1.3 billion cash balance is tagged as "Softbank Warrant Proceeds received on October 30, 2019." Interestingly, this extra amount was not included in the previous slide as of December 31st (shown below) that WeWork provided to Softbank as of February 12 when Softbank reported its third-quarter earnings:

This $100-200 million difference is important, therefore, because it appears to be all the cash WeWork actually had available to spend as of December 31st. Which meant WeWork burned through all of the $1.5 billion emergency cash Softbank wired in October 22nd plus most if not all of approximately $270 million I estimated it had actually available in cash to spend as of September 30th—indicating at least $1.8 billion consumed.

That $100-200 million likely is long gone, along with most if not all the $800 million in restricted cash WeWork was able to free up after Goldman Sachs Group (GS US) finally agreed to complete in February (after a strange and unexplained delay) the $1.75 billion letter of credit facility it arranged back in December on the condition that Softbank would sign on as co-borrower (to the alarm of Softbank's banks).

Which makes it laughable that WeWork expects to burn through only another $2.5 billion by 2022, as shown in the slide above it gave to Softbank in February.

We can also see in slide #1, shown first above, that $1.1 billion Softbank previously had committed in "secured debt financing," and which WeWork previously counted in pro forma cash as recently as the slide to Softbank on February 12th, now is tied to the completion of the tender and may not happen.

I suspect that the $2.2 billion still listed as unsecured loans soon to be funded from Softbank also remains in jeopardy. The fine print in the footnote reveals that Softbank requires significant conditions before this cash can even be drawn, and the offering seems to be indefinitely delayed at best. Now, as I have speculated, pulling the tender set in motion events that could lead to Softbank walking away from the entire takeover deal—and this loan too.

If so, WeWork's already fraught situation may become untenable almost immediately. Without substantially more cash, financial viability, or credible proof that it can complete even existing agreements, WeWork may find it nearly impossible almost immediately to continue to do business at all.

I also imagine WeWork has considered this a likely contingency for several months and is prepared to file bankruptcy at any time, leaving its bonds nearly if not completely impaired and its equity worthless.

I have warned for months that risk for WeWork bonds remains acute. The bonds were down another 2 points since last week to 35.3 (37% ytw; 3665 bps) and are down 54 points since my report on March 18th. Substantial downside risk remains given my estimate that the bonds may be as much as 100% impaired. I continue to expect WeWork will pursue a comprehensive capital restructuring, bankruptcy, or even liquidation unless the company can renegotiate as much as $50 billion locked up in expensive long-term leases WeWork can't afford—which seems unlikely. Given its dire prospects plus nominal tangible assets of limited quality, upside potential from a near-term rebound in operations or business conditions or company sale seems unlikely. Maintain “Sell.”

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.