Look Away From Elon Musk To Gauge Tesla's Prospects—and Looming Risks

Sure the Elon Show is on all channels, but he and Tesla did have a very good year. They also caught a lot of lucky breaks that won't last—which is overlooked by investors. Next year will be different.

Who doesn’t already know, or still needs to know, that Tesla’s bombastic CEO Elon Musk is the richest man on the planet?

That he and his adoring fans burn hot for his relentlessly prolific publicity mostly concocted by his deliberately outrageous antics? That he is—true or (often) not—an authority on most worldly topics (just ask him)? That he’s a rarified genius—or a audacious charlatan with an ego as massive as it is fragile?

We get it. He and Tesla have had a very good year.

Also true: Musk and Tesla caught a lot of breaks which greatly facilitated their good fortune. Like Musk selling all his houses he bought for $100 million in California and moving to Texas to slash his tax bill. Like then telling the world he was “selling almost all physical possessions” and “will own no home” and living secretly most of the time in his buddy’s multi-million dollar mansion in Austin versus the modest $50,000 house in Boca Chica he told the world was his “primary home.” Like convincing his fans it was their idea for him to sell 10% of his Tesla stock ($13 billion so far) to pay for his tax bill, even after he announced last September that he needed to sell stock to cover expiring options. Musk, who has rarely paid taxes at all, also wailed that his tax bill was unfair despite every penny of profit Tesla has reported and, as a result, virtually his entire fortune, being traced to billions in taxpayer-funded subsidies.

Tesla’s rivals also incurred heavier disadvantages and higher costs from industry supply disruptions compared with Tesla’s reported results. Of course, Tesla also “repurposed” chips to cut costs, rewriting chip software to support other functions, or just dropped features and equipment supported by chips it couldn’t get—without always telling Tesla owners and buyers who paid dearly for features they didn’t have.

Cue future recalls and other related problems. Given Tesla’s famously poor track record with software fixes on the fly for its controversial Autopilot FSD Beta I have low confidence in the efficacy of Tesla’s chip rewrites. Similarly, Tesla has diminished Autopilot capability by dropping radar because, Musk claimed, radar actually reduced safety versus an all-camera system.

Musk had repeatedly told members of the Autopilot team that humans could drive with only two eyes and that this meant cars should be able to drive with cameras alone.

Inside Tesla as Elon Musk Pushed an Unflinching Vision for Self-Driving Cars,

The New York Times, 12/6/21

I’m not buying Musk’s disingenuous and naively simplified solution. We humans drive using our eyes, our ears, our depth perception, as well as our brilliantly complex human brains—a combination far superior to Tesla’s system which was seriously flawed even with radar.

I say Musk cut radar capability to slash costs, probably the same reason he refuses to use lidar, leaving Autopilot critically and fundamentally impaired as a result.

Also concerning has been the increasing incidence of Tesla’s forced and “encouraged” recalls of cars. Moreover, recalls executed by Tesla in one market are not carried forward into other markets where the same targeted cars had sold.

Not to mention that Musk and Tesla continues to get by with stretching, and even apparently shredding the truth about their promises and problems—as they have for years.

Indications are that Tesla’s long stretch of luck and lavish indulgence may be coming to an end. Musk’s billions, brags, insults, and rants have overshadowed growing concerns that can’t be ignored for much longer, like struggling Model 3 same store sales trends I’ve been tracking for years. Like Tesla’s shrinking market share in key markets from robust competition winning buyers spooked by its own notoriously poor build quality in it cars plus its dismal customer service. Like eroding margins from seemingly inflated levels which likely will worsen through next year.

Add emerging consequences from Tesla’s notorious false and misleading full-self-driving (FSD) claims, sneaky “fixes” of serious problems instead of recalls as required, dicey accounting, increasingly significant recalls as years of shoddy manufacturing and apparent coverups are revealed, and escalating government probes may expose all manner of ugliness to the world.

I long have projected that many, if not all of these negative factors may begin to coalesce next year, particularly in the second half. If so, Tesla could struggle increasingly versus record results this year.

Yes, Tesla is closing its best year yet. Or its peak year. We’ll see.

First, some good news.

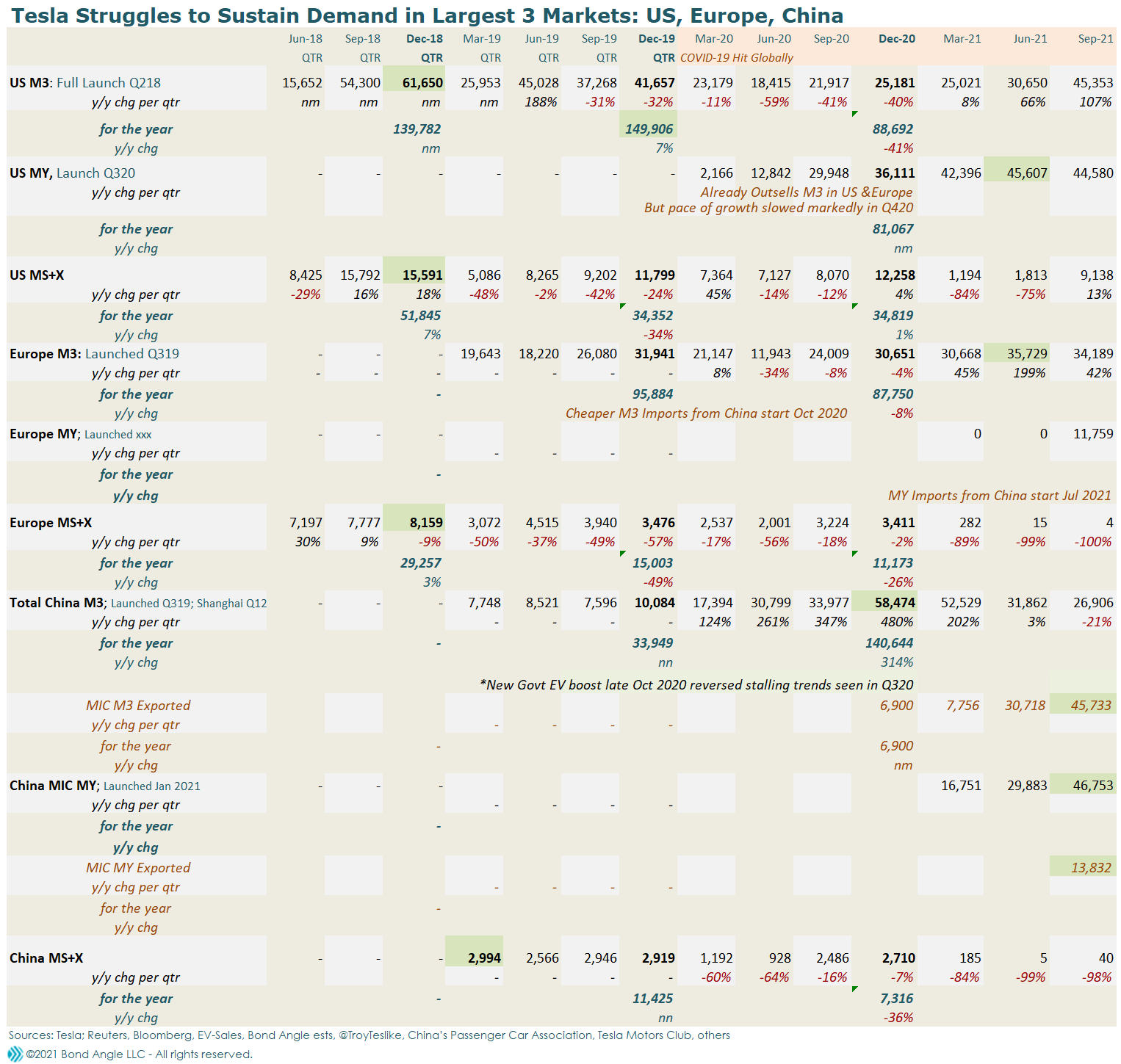

Tesla is expected to report fourth quarter deliveries early next week. Market consensus projects 285,000, up 58% versus last year. This includes 273,000 in Models 3 & Y.

That’s higher versus my estimate for 255,000 (up 41%) including 242,000 Models 3 & Y. I expect the difference may be better than expected sales in Europe of the newly available cheaper Made-In-China (MIC) Models 3 & Y, which I see as a comparatively short-term surge.

Otherwise, the story to watch is the continuing plunge in Model 3 sales in China—the largest EV market in the world—versus Model Y, as well as Tesla’s shrinking market share overall versus robust rivals like Chinese giant BYD (1211 HK) and local EV startups Lixiang, Xpeng (XPEV US) and NIO Inc (NIO US).

Similarly, Tesla is losing share overall in Europe to Volkswagen (VOW GR) and others, and this is before it gets new Berlin-based capacity online (now delayed again into next year).

MIC Model 3 sales were down a whopping 74% y/y in China the first two months of the fourth quarter, and down by high double-digits in 5 of the past 7 months through November. By comparison, China industry EV sales have jumped by triple-digits y/y in each of the past several months.

Loss of staying power is not new for Tesla—I’ve been tracking it since 2018. As I wrote last in Tesla Model 3 Sales Crashed in China in October:

Apparently folks haven’t been paying attention because, as I long have warned clients, Tesla has been losing ground in China for most of the past year—longer than that for MIC Model 3:

Indeed, MIC Model 3 deliveries in China were tracking lower y/y all during the third quarter versus expanding sales of MIC Model Y, which launched in the first quarter. I anticipate a similar pattern to develop in Europe now that Model Y has been introduced there as of August:

This, as I have noted before, is the same pattern I’ve been tracking for years. Sales in Tesla’s legacy models have faded almost immediately when faced with its new models, and now Tesla is facing stiff new competition from strong rivals in all its markets—especially China. Its new models have also struggled to sustain sales after initial new launch and/or new market expansions, sometimes even before the first anniversary of said events (I last discussed this at length in Tesla: Don’t Drive Angry, 2/8/21).

Tesla's August Sales Numbers in China Don't Add Up, 9/17/21, followed up with Tesla: Now That's More Like It on 10/15/21 and Looks like Tesla MIC Model 3 Deliveries in China Fell Sharply in Q3, As I Warned on 10/4/21.

If past trends hold as they have for Models 3, S, & X, I expect Model Y sales momentum may begin to fade sometime next year.

And unlike Tesla’s strong and growing competition in every major market, Tesla’s fleet is several years old now and it has no credibly new models ready to launch at scale to capably meet the assault. Certainly not the quirky boy-toy Cybertruck, which already pales versus the newly launched Rivian (RIVN) R1T and the eagerly received Ford (F) F-150 Lightning. That’s lost ground which likely will stay lost.

But that’s a problem for next year, which starts in two days.

Tesla repurchased its 5.3% senior notes in the third quarter as I projected, though I doubt we’ve seen the last of Tesla as a bond issuer:

Now stay tuned for the second step I described: a quickly shopped, likely $2-4 billion inordinately low coupon bond deal, accompanied by a bump in credit quality ratings potentially to low investment grade (see Tesla's Car Business Finally Turned A Profit. Really. Time For A Big Bond Deal). It could even be appealing... if it’s priced at T+100 bps or better.

Until then, I have Tesla: Not Rated.

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.