Tesla: Don't Drive Angry

Tesla’s Q4 deliveries confirmed its 2-year struggle with falling core demand continued through Q4. Don't look now but Serious Competition Is Here. Part 2 of 2 after Tesla: The Sky's The Limit...Until

Last Wednesday marked Groundhog Day for Puxatony Phil and Tesla (TSLA).

Phil saw his shadow which means six more weeks of winter—as usually happens. Similarly, here we are chewing again over how much padding was in the numbers Tesla (TSLA) reported in fourth quarter results—as has happened in every quarter for years.

Sure enough, there was more than enough just counting the $401 million in energy credit sales (up 202%) to mask yet another sizable loss so Tesla could report “profit” as has happened in each of the previous five quarters (as I projected in the first part of this 2-part series Tesla: The Sky's The Limit...Until on 1/25/21). We’ll know more after Tesla releases its 10-K filing.

Unfortunately, Tesla still trailed market expectations with just $270 million in reported net income (and dramatically worse unvarnished loss) despite substantially higher revenue up 46% y/y to $10.7 billion, (see Tesla: Oh No You Didn’t on 1/28/21).

But Tesla has bigger problems than missed earnings. Tesla’s fourth quarter deliveries confirmed disturbing demand trends I have tracked for more than two years (and most recently detailed again in What’s Going On With Tesla’s Demand? on 10/27/20).

Regardless of its marketing hype, it’s obvious Tesla knows this too. But so far it has failed to curb the threat which now affects all its models in every market even as it rapidly escalates expensive production capacity. This comes as 2021 becomes the first full year Tesla actually will face a broad slate of serious, and aggressively winning, competition.

No wonder Tesla was uncharacteristically cagey about its prospects for 2021 and beyond.

It’s Really Just All About Deliveries

Tesla’s fourth quarter deliveries were 180,667, up 61% y/y and several hundred short of the quarterly tally needed to meet the company’s long coveted goal of 500,000 for the year.

Not surprisingly, aging Models S & X deliveries were down another 3% versus last year when they dropped 29%, marking eight down quarters of the past nine.

Models 3 and Y were reported up a whopping 75% to 161,701—but hold the confetti. All of that growth came from the launch of Model Y and the ramp up of Made-In-China (MIC) Model 3 in China. Moreover, MIC Model 3 sales were stalling until a new government-backed incentive kicked in—which appeared to help Tesla’s competitors even more.

In other words, sales trends were much weaker than Tesla wanted us to believe.

Indeed, I suspect Tesla may have been more surprised than we were that it came in so close to 500,000 deliveries. After all, the company had promised in 2016 to hit 500,000 by 2018 and 1 million cars by 2020.

Fast forward to early 2020, when Tesla had remained steadfast that it would deliver “comfortably above” 500,000 cars for for the year regardless of COVID-19 impacts or other emerging disruptions. It wasn’t until late in the third quarter that Tesla, surprisingly, hedged its outlook.

At the shareholders’ meeting in September, CEO Elon Musk amended guidance to 477,950-514,720 deliveries for the year, up 30-40%. Most of the wider projected range fell well below 500,000, versus “comfortably above,” with the midpoint indicating roughly 496,340 (up 35%) for the year.

The revised outlook indicated a range of 159,000-196,000 (up 44-77%) for the quarter with a midpoint at 177,235 (up 58%), still well above market consensus of 163,000 but closer to my 175,000 estimate.

So the result of 180,667 ultimately reported may look like a modest beat versus lowered expectations, but it really was a lucky save which added at least 20,000 units to the total thanks to a new EV-friendly policy implemented by China in late October.

As I noted in Tesla to Sell Another $5 Billion in Stock—Might As Well on 12/8/12:

Fourth quarter trends so far indicate more of the same weakness in the US and Europe noted in the third quarter, but Tesla caught a break in China at the end of October when the government implemented new ICE restrictions which effectively boosted sales of EVs.

So instead of scrambling to find sales for production out of its new Shanghai plant, including shipping 7,000 Made-In=China (MIC) Model 3s to Europe (where they apparently aren't selling any better) Tesla's China sales doubled versus estimates to 22,000 in November.

December monthly China sales were better but below estimates at 23,804 for MIC Model 3. Why? Because that boost to EV sales from the China policy change helped all EV sellers there—including leaders already outperforming Tesla.

The truth is Tesla has been losing market share in China for months to local automakers, losing its top ranking in monthly sales in August despite multiple rounds of aggressive price cutting. Bad news considering China sells 40% of all EVs in the world.

And while Tesla may claim it was production-restrained, it reportedly was producing more than 5,000 cars per week from its Shanghai plant—more than sufficient versus sales. Recall my concerns that Tesla had so much excess inventory it began to ship MIC Model 3s to Europe in October (see What’s Going On With Tesla’s Demand? on 10/27/20) even though it previously had boasted it would need several plants just to meet demand in China. Not to mention quality concerns with MIC Model 3 becoming amplified in Europe versus higher quality German-made rivals, for example.

Past trends suggest the next threat to MIC Model 3 sales in China will come from Tesla’s Model Y, which it began delivering there three weeks ago after it initiated a 31% price cut even before the first car arrived in stores. This followed yet another severe price cut on MIC Model 3 by 8% in October, marking seven sizeable price reductions for the year.

So much for “insane demand”, as Elon likes to say.

The same may also be proven true in Europe, the largest EV market in the world in 2020 where Model 3, already knocked decisively out of the top monthly sales rankings as of May, continued to lose market share to Volkswagen, Renault, Hyundai, Audi, Smart EQ, and others, as I projected in What’s Going On with Tesla’s Demand?.

And this was before full ramp-up of many of the newest models launched last fall, with dozens more on the way.

Tesla, we’ve seen this before.

This pattern of surge, falter, and urge with expensive price cutting and incentives has characterized Tesla’s sales in all its models for more than two years, as I detailed again in What’s Going On With Tesla’s Demand? on 10/27/20.

So far, the strategy has failed to sustain same-store sales for any of Tesla’s existing models in all its major markets: the US, Europe, and China. Since 2018, Tesla has relied exclusively on incremental sales growth via new models and model expansion into new markets, plus now a new plant in China, for all its sales growth.

As a result:

Model S & X sales peaked in Q218 when Model 3 launched at full scale in the US, long Tesla’s primary market;

US Model 3 sales peaked just two quarters later in December 2018 and have been in decline y/y ever since;

Model 3 sales in Europe peaked in four quarters as of December 2019 and have been in y/y decline the past three quarters;

MIC Model 3 sales stalled by the third quarter of its first year, even after six price cuts by September 30th and seven for the full year. Sales were reiginited only after China implemented another generous EV-friendly policy (which helped all its competitors as well). But…

Odds are that MIC Model Y curtails MIC Model 3 in China just as it did in the US—and as it likely will in Europe.

And if past trends hold, Model Y sales could start to fade in the US by the third quarter this year.

Forecast for 2021: Foggy

Deliveries were up 36% for the year at just under 499,650, mostly on the 47% increase in Models 3 & Y to 442,560. Demand was comfortably met with production up 40% to 509,740, mostly on the 51% increase in Models 3 & Y to 454,930.

By year-end, plant production capacity was up 78% to more than 1 million units—and counting as additional production is ramping up for Model Y at both plants. This is on top of similar production capacity to be added over the next year with plants now under construction in Texas and Germany.

Considering that Tesla is losing market share at an accelerating rate in all these markets, which likely will continue through 2021, it seems like Tesla is creating substantial overcapacity versus demand for potentially several years.

Perhaps this explains Tesla’s surprisingly vague guidance for deliveries in 2021 and beyond:

We are planning to grow our manufacturing capacity as quickly as possible. Over a multi-year horizon, we expect to achieve 50% average annual growth in vehicle deliveries. In some years we may grow faster, which we expect to be the case in 2021. The rate of growth will depend on our equipment capacity, operational efficiency and capacity and stability of the supply chain.

Tesla Q4 and FY 2020 update.

This, I take it, indicates Tesla expects something better than 750,000 deliveries for 2021, dramatically lower versus Elon Musk’s projection in the Q3 2020 earnings call that 840,000 to 1 million “was in the vicinity.”

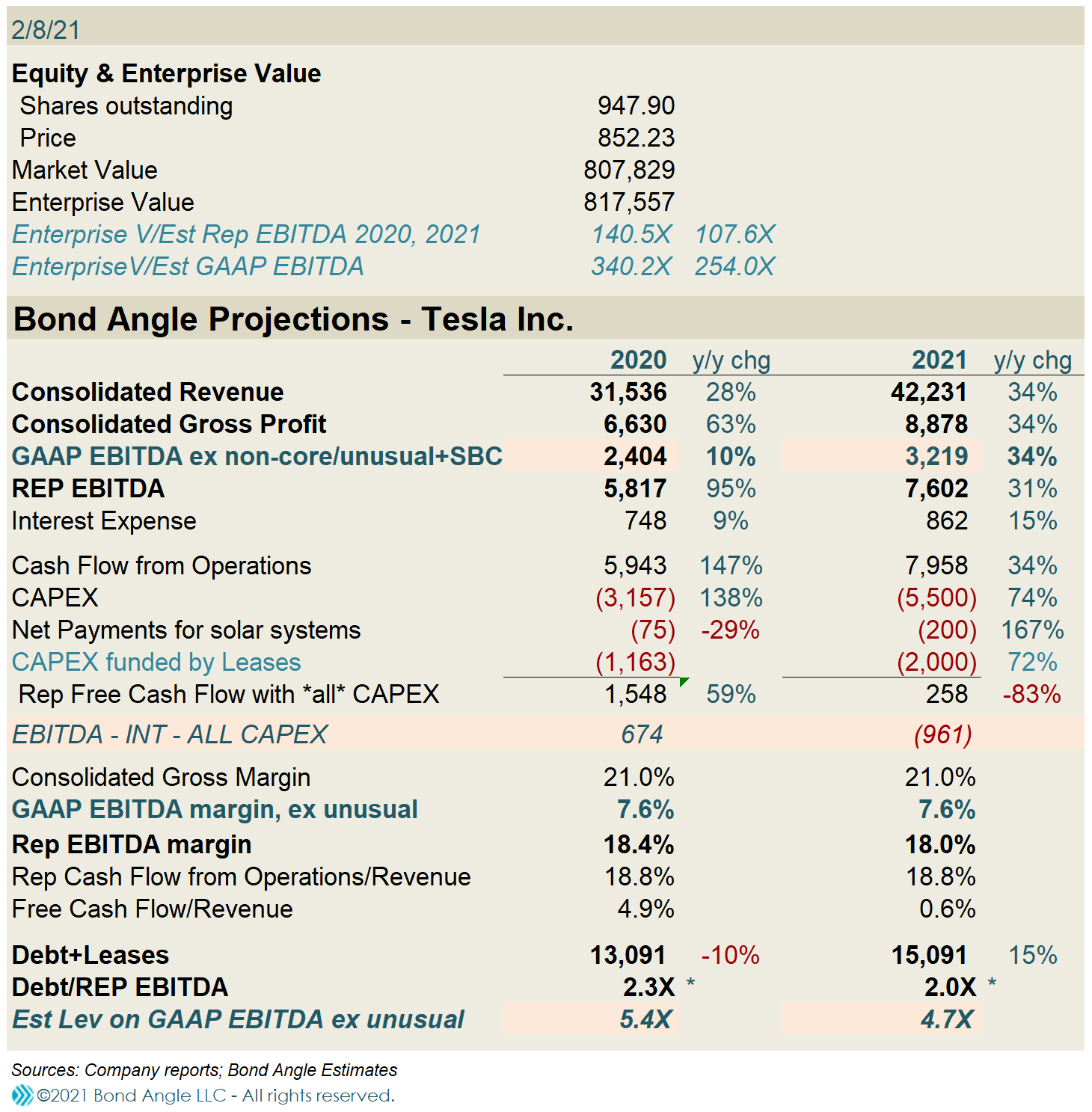

Interestingly, the market seems to be comfortable barreling ahead with Musk’s dramatically more ambitious old guidance. How else to justify Tesla’s $800 billion market cap, its 1200x trailing P/E ratio & 206x forward P/E (which assume generous consensus estimates) for a company that has yet to generate unvarnished profit or free cash flow on core operations in 17 years and was only able to plump up its balance sheet by selling more than $12 billion in stock at drastically inflated prices? (see Tesla: Oh No You Didn’t on 1/28/21).

Nope, I can’t get there (see Things People Believe: Flat Earth, Faked Moon Landings, and Tesla $2100 on 8/23/20).

No worries, Elon Musk still claims Robotaxis can drive Tesla to $1 trillion in market cap! Still no, Elon. Even if this capability did materialize fully formed in the next few years, and this I seriously doubt, the concept still is even more years away from getting local, state, and federal approvals or universal backing from insurance carriers (see Tesla “Autonomy Day” Takes Investors For Another Ride on 4/24/19).

On top of that, Tesla’s Autopilot remains far less safe and capable than advertised. Regulators still are investigating ongoing Autopilot-related injuries and deaths and Smart Summon which Consumer Reports declared an expensive "science experiment" that was "glitchy" that worked "intermittently, without a lot of obvious benefits for consumers."

So we’re left with evaluating demand, and trends I have tracked suggest demand will remain more pressured for Tesla versus mostly optimistic market estimates.

I assume continued erosion in the US and Europe for Models 3, S, & X, with primary growth from Model Y in the US, Europe, and China, and stalling MIC Model 3 as MIC Model Y takes hold. I assume only modest sales at best from Cybertruck and Semi-Truck launches later in the year, if at all. I estimate roughly 154,000 deliveries for the first quarter, down 15% vs the fourth quarter and up 74% versus Q120, and nearly 768,000 (up 54%) for the year.

If so, this indicates revenue for the year at $42.2 billion (up 34%), reported EBITDA at $7.6 billion (18% margin), GAAP EBITDA excluding unusual/nonoperating & other items at $3.2 billion (8% margin), and leverage on unvarnished EBITDA near 5x.

I’ll publish a full model with adjusted historical results and projections after Tesla releases its 10-K filing.

Tesla's 5.3% senior notes due 2025 are little changed since my last report at 104.2 (2.5% ytw; 204 bps), offering no credible upside versus potentially significant downside. The bonds remain excessively valued with yield tighter by 173 bps versus the BoA High Yield general index even though Tesla is a weak B3/BB- issuer. Pricing also indicates a meager 68 bps per turn of leverage on my estimated 2020 reported EBITDA and an appallingly low 37 bps per turn of leverage on core operating—unvarnished—EBITDA. Maintain "Underperform."

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.