Tesla: Looking For Trouble

While Waiting To Get Court Approval Of His Sweet Deal Granted By The, CEO Elon Musk Continues To Insult The SEC

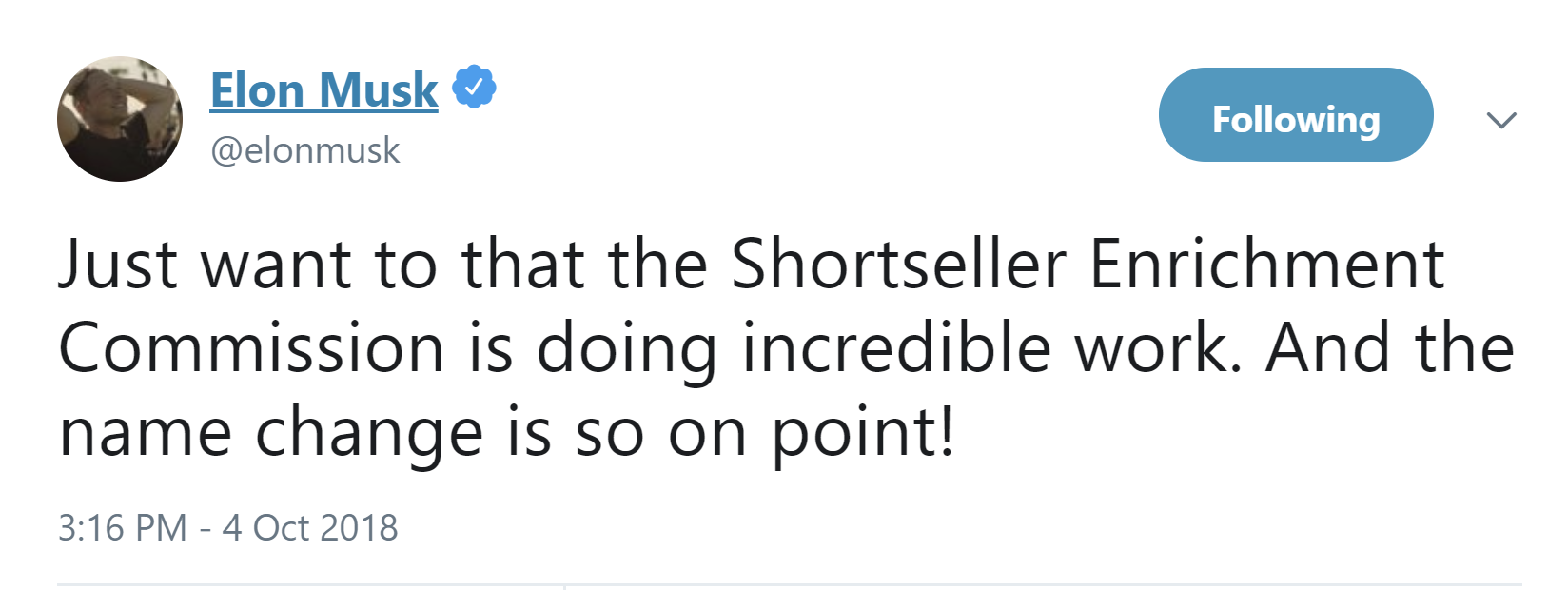

Tesla Motors (TSLA US) stock fell as much as 4% in after-hours trading because CEO Elon Musk again insulted the Securities and Exchange Commission, this time by posting a nasty tweet after the market closed in which he called it the "Shortseller Enrichment Commission."

Yes, he did.

I warned last week that the generous deal the SEC gave Musk and Tesla didn't go far enough to address serious management deficiencies.

The federal judge charged with ruling on that proposed settlement may come to agree, especially after Musk's latest stunt.

Cringeworthy drama continues

Musk continued to insult the Securities and Exchange Commission, this time by posting this nasty tweet after the market closed:

He pulled this latest stunt just hours after a federal judge with the Southern District of New York began to evaluate whether his generous settlement with the SEC is a suitable and effective punishment for his securities fraud and reckless communications promoting his bogus buyout scheme via tweetin August (see my reports "Musk Fought the Law and the Law Won—So What?," Tesla Take-Private Plan: Shoot First, Answer Questions Later (If at All)," and "Tesla’s Take-Private Plan: Never Mind").

Judge Alison Nathan did not approve the settlement. She said the Court's duty is to ensure the settlement is "fair and reasonable" and that it "furthers the objectives of the law upon which the complaint is based." She ordered Musk, Tesla, and the SEC to come back in one week with a joint letter explaining why she should approve the remedies and penalties proposed.

That's a good question. Musk can't even abide by the part of the deal requiring him to comply with designated oversight on his communications, specifically:

"All mandatory procedures implemented by Tesla, Inc. (the “Company”) regarding (i) the oversight of communications relating to the Company made in any format, including, but not limited to, posts on social media (e.g., Twitter), the Company’s website (e.g., the Company’s blog), press releases, and investor calls, and ii) the pre-approval of any such written communications that contain, or reasonably could contain, information material to the Company or its shareholders"...

Securities and Exchange Commission vs. Elon Musk; Case 1:18-cv-08865-AJN, Document 6-1 Filed 09/29/18

This especially applies to snarky tweets that may enrage the SEC, the Department of Justice, and federal judges who are deciding right just how much/what kind of penalties to assess.

Indeed, the judge might cite Musk's tweet as a good example of why the settlement doesn't go far enough to address serious management deficiencies with Musk and Tesla that have and will continue to harm shareholders--as I noted last week--and recommend tougher penalties, perhaps even Musk's removal as CEO.

After all, Tesla stock dropped another 4% in aftermarket trading to $273 per share, but what's another $1.4 billion in evaporated market cap among friends.

Musk can't seem to grasp that when he demonstrates such dismal regard for regulators who actually gave him a huge break when he was in the wrong, why then should anyone believe he has genuine respect for obligations and responsibilities to suppliers, customers, creditors, employees, or investors who all are being impaired because of Tesla's difficulties directly caused by his failings.

They also comprise the vital support he must have if Tesla is to successfully navigate serious financial pressures it faces over the next year (see my forecast in"What Tesla Can Learn From Navistar About Arrogant Management, Serious Mistakes, and Survival").

Moreover, as I warned last week, serious criminal investigations into Tesla continue and those investigators are no doubt paying close attention to Musk's belligerent behavior. So are shareholders who have filed numerous lawsuits alleging securities fraud. They have no reason to trust him.

However, given Musk's controlling lock on Tesla's entrenched, insular board, the most necessary changes probably will have to be forced either by regulatory action via penalty mandates or, less likely, an aggressive assault by a commanding block of Tesla's largest investors.

Here again are my recommendations, as previously presented last week:

Musk must not choose Tesla's new chairman. Tesla's new chairman must be a truly independent, seasoned auto industry veteran who can demonstrate management strength, operating prowess, and help begin to restore the company's shredded credibility.

New directors Tesla is compelled to add must be truly independent, and the company should increase its board to at least 12 directors to ensure demonstrable management oversight.

Tesla's board should create and publish and enforce new standards for management oversight, accountability, and public communication.

Tesla must install and retain a broad-based bench of seasoned auto industry veterans who can help Musk lead and help Tesla execute its critical transition into a sustainable carmaker. Better-healed rivals are bringing strong competition for 2019.

Tesla needs to replace and retain top-flight accounting and finance execs to ensure there are no worrisome financial irregularities. If there are problems, get them fixed and install appropriate compliance and controls before the year closes for audited financial statements. Too many high-level finance folks leaving too frequently have raised serious concerns.

Getting seasoned, credible management in place early can head off problems and damaging fallout later. Bolstering its finance team also can help ease growing concerns from Tesla's wary suppliers, creditors, bondholders, and investors that the company can appropriately manage its troubling liquidity pressure and the potential need for additional funding while it navigates at least three more difficult quarters before the company becomes convincingly self-sustaining.

Musk destroys goodwill these days as effortlessly as he breathes air.

He's also demonstrated time and time again that he serves his own interests over everything else. As I have observed before, if he continues to harm the company he must go.

While investors may worry and the stock may suffer initially as a result until the company is stabilized, and it will stabilize, Tesla can move on without Musk—and it probably should.

Tesla desperately needs a capable CEO who is most interested in running a car company. There are seasoned industry veterans who can successfully turn around a foundering carmaker, build a deep bench of strong management, run efficient manufacturing, sales, and delivery operations, and make beautiful electric cars consumers are excited about.

In fact, formidable new rivals are already on their way over the next several months and into next year; e.g. Mercedes-Benz EQC 400 4Matic, the dazzling Jaguar I-Pace, BMW’s iX3 SUV, Porsche’s Taycan, and the Audi A3 e-tron followed by a new Q8 SUV.

Buyers for those cars don't have to worry about zany high jinks the CEO might pull—or whether the company will be around long enough to service their warranties.

I remain wary that Tesla will fall short of management's guidance and market estimates for third-quarter results. Maintain “Underperform” on TSLA 5.3% Senior Notes due 2025, down nearly 2 points over the past 3 days to 86 (7.9% ytw; 480 bps). Given Tesla's persistently volatile situation we still could see 3-5 points additional downside from here.

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.