Tesla Q219 10-Q Notes and Big Red Flags

Tesla's Q2 10Q fills in worrisome gaps and raises troubling concerns, including why Telsa founder JT Straubel really left.

Tesla filed its 10-Q for the second quarter on Monday which, as usual, raised new questions and concerns without really filling in all the gaps in disclosure left hanging after its disappointing earnings report last week (see "Tesla Q2 Results: Diminishing Returns").

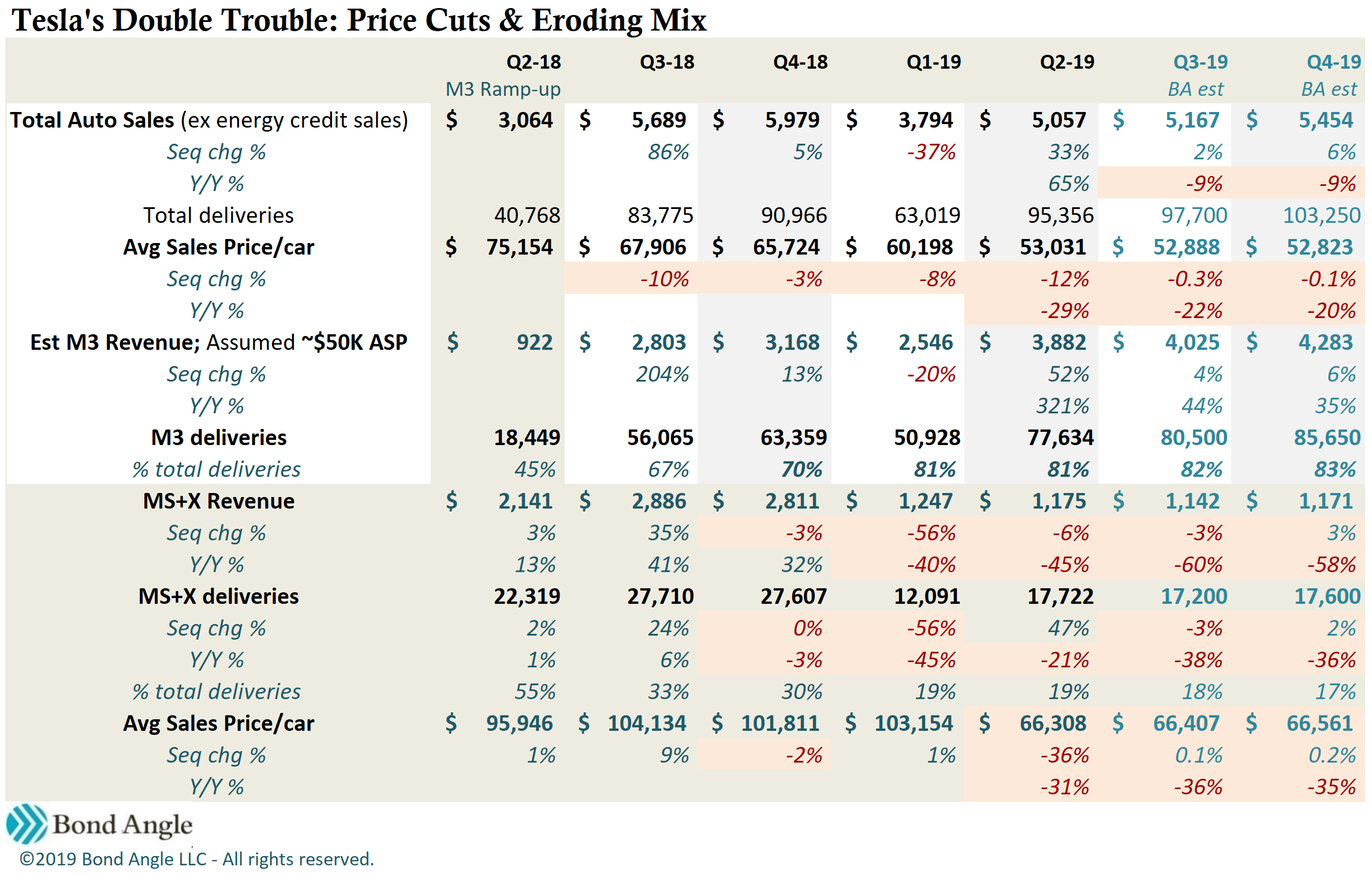

I warned again in Tesla Q2 Deliveries Beat; Demand and Profit Trends Less Clear that underlying demand trends in 2019 have been marked with escalating weakness that drastic pricing discounts haven't fixed. The 10-Q revealed more clues that Tesla may have needed another white knight to land its record second-quarter deliveries at the last minute, likely at severe price discounts.

Tesla ended the quarter with a big increase in cash, but the 10-Q confirmed my concerns that operations actually generated almost none of it—again. This is bad news given Tesla's sizable and still unsupported cash drain in operations every quarter plus its massively underfunded pipeline obligations—including one likely expensive surprise project it's yet to disclose.

We also learned what Tesla sacrificed to get the Shanghai factory deal in China and how it could lose it all.

One critical loss Tesla will suffer more immediately is JB Straubel, longtime Chief Technology Officer and the company's last co-founder besides CEO Elon Musk, who surprised the market last week by announcing he is leaving. An amended agreement with Panasonic disclosed in the 10-Q offers hints about why now, after sixteen years of helping to build a company he clearly loved, Straubel decided to leave as Tesla is supposedly on the brink of fruition with so many vital projects under his stewardship.

Questions. We have questions.

I was concerned in "Tesla Q2 Results: Diminishing Returns" that "accounts receivable was up another 10% versus the first quarter and up 101% versus last year—again outpacing the 59% y/y growth in consolidated revenue. Tesla's bloated accounts receivable remains a curious mystery for a company that operates by requiring cash upfront from customers before their cars are delivered."

The 10-Q disclosed that "as of June 30, 2019, one entity represented 10% or more of our total accounts receivable balance" which ballooned to $1.15 billion. This means one "entity" owed roughly $130 million, and likely much more, just as the quarter came to a close.

This happened once before in Tesla's "miracle" third quarter (see Great Magic Trick Tesla; Now Do It Again). Tesla had been concerned up to the last day of the quarter that it would miss guidance by failing to report its first profit in years, with Musk emailing to employees "We are very close to achieving profitability and proving the naysayers wrong, but, to be certain, we must execute really well tomorrow."

As I observed then, "very close" to profitability means not profitable the day before the quarter closes, signaling Tesla has a "very" good chance of missing guidance." Instead, accounts receivable nearly doubled versus the previous quarter, helped by an "entity" which claimed more than 10% of the balance due. Tesla remained cagey but indicated the entity was a bank that hadn't completed loan processing on last-minute car sales, which I estimated as potentially 10% of total cars delivered for the quarter.

Not only did Tesla's feeble explanation account for less than half of the total jump in accounts receivable, but it's not clear how much was later collected. Whether or not the balance of the late transactions came from last-minute fleet sales—likely at discounted prices—accounts receivable have remained elevated ever since and have grown significantly faster than revenue for two straight quarters.

For this quarter, Musk emailed to employees that "record" deliveries were "very close" but still not there a week before the quarter closed. In this case, record deliveries meant topping 90,966 in the fourth quarter but, as I had pointed out, Tesla actually needed to deliver 99,000-112,000 to get back on track to meet guidance of 360,000-400,000 for the year after disastrous first-quarter results (see Quick Take on Tesla Q119 Deliveries: Yes, They Were Bad).

Right on cue, another unnamed "entity" stepped up at the last minute with a big purchase, this time at least $130 million to, more likely, closer to $200 million or, say, $45,000-50,000 per delivered car. Why so much? Well, as of June 25th Tesla had delivered less than 91,000 for the quarter, as indicated by Musk's email. And over the next week, Tesla managed to come up with just over 4,000 deliveries to bring the total to 95,536.

It's not a stretch to assume pricing was heavily discounted for such a desperately needed last-minute sale, with the average price per delivery down to $53,031 for the quarter.

That's down 29% y/y and down 23% versus the third quarter—the last time Tesla needed an 11th hour white knight to make its numbers for the quarter.

How did Tesla generate so much free cash flow despite a huge net loss? It didn't.

Tesla ended the quarter with $4.95 billion in cash but, as I reminded investors in my last report, most of the $2.75 billion increase versus the first quarter came in May from $848 million sold in stock and more than $2 billion sold in bonds (see Tesla: When a Spartan Diet + $2 Billion Isn’t Enough).

Tesla pointed to $614 million in free cash flow but, as in previous quarters, most of this was not actually cash generated from operations. As I've already noted, most of the $864 million reported in cash flow from operations can be traced to $965 million in noncash charges (depreciation, stock-based comp) and "other" line items plus a nominal working capital gain, offset by the surprising $408 million net loss. Reported free cash flow also was boosted by another severe reduction in capex to just $250 million—down $360 million versus $610 million reported last year.

The 10-Q disclosures better differentiated operating versus nonoperating and unusual cash sources. The chart below identifies many previously undefined line items which boosted cash and shows how much additional cash Tesla raised from borrowing and other miscellaneous nonoperating sources. This included a return of some of Tesla's deposit for commencing construction on the Shanghai factory plus cash Maxwell Technologies had on hand when Tesla closed the acquisition in May:

So, striking out most all unusual items, as shown above, indicates Tesla's operations generated barely breakeven cash—a far cry versus the $614 million in free cash flow Tesla reported. This is a familiar pattern by now. Indeed, roughly a third of the $1 billion shown above in estimated available cash for the first quarter also came from borrowing and unusual, nonoperating items (see Tesla: When a Spartan Diet + $2 Billion Isn’t Enough).

Given my forecast for revenue declining in the second half versus last year, with lower margins and continued losses, a strong rebound in free cash flow doesn't seem likely. Tesla wasn't able to generate sustainable, unvarnished free cash flow even when it reported profits in the third and fourth quarters last year when revenue quality and operating margins were significantly stronger (see my reports "Great Magic Trick Tesla; Now Do It Again" and "Tesla: Down to the Wire").

We've seen how Tesla's chronic liquidity pressures have driven severe and even ill-advised cost-cutting strategies that hurt sales as well as quality and reliability in its cars—which hurt profits. Tesla's likely expectation that cash flow generation will continue to be a problem helps explain why it starves R&D and capex even as its expensive pipeline becomes so seriously delayed and compromised that demand and market share are threatened—and even when it sits on nearly $5 billion in cash.

More Shanghai Surprises

One of those projects is Tesla's new factory under construction in Shanghai since January. In my report "Tesla - Shanghai Surprise" I warned that Tesla had launched into building the factory without first getting funding arranged when most projects of this size have financing firmly in place long before construction starts.

I warned that Tesla's persistently weak financial condition, its seriously depleted liquidity, its inability to provide sufficient collateral, and its long track record of poor execution made the company a poor credit risk for its Chinese lenders. Starting construction on the plant anyway severely weakened its bargaining leverage.

Sure enough, as I noted in "Tesla: Now We Know the Y But Not the How," "it took months for Tesla to finally secure a loan from local Chinese banks as promised to fund its Shanghai factory. Even then the wary bankers only agreed to [just over] $500 million in short-term, limited purpose financing, barely enough to get the factory up and running—much less versus the more than $2 billion it will cost to build out the factory even to half its projected 500,000 car annual capacity (although indications suggest demand may be far lower by the time the factory is completed)."

Now, seven months after Tesla broke ground on the plant, the 10-Q has disclosed:

The plant will cost at least $2 billion to build, as I projected. This according to its operating lease arrangement, finally disclosed in the 10-Q, in which it agreed to spend RMB 14.08 billion in capital expenditures over the next five years.

The agreement also requires Tesla to “pay annual tax revenues of RMB 2.23 billion”—nearly $324 million in current US dollars—to China starting at the end of 2023. Uh oh—Tesla hasn't generated a single profitable year in its sixteen-year history even after now three quarters of record deliveries.

If Tesla is unable to comply, it could lose the plant altogether:

"If we are unwilling or unable to meet such target or obtain periodic project approvals, in accordance with the Chinese government’s standard terms for such arrangements, we would be required to revert the site to the local government and receive compensation for the remaining value of the land lease, buildings and fixtures."

While construction on the plant is nearly complete, Tesla still is lacking "manufacturing licenses" or "regulatory approval" to commence production. This adds to concerns raised in other reports that the Shanghai plant is going up in less than half of what would be a record building time of 17 months. Feng Shiming, executive director of Menutor Consulting Shanghai, told the Global Times, "the factory's construction pace is too fast, which is set to leave some problems such as insufficient equipment testing and staff training."

Tesla has yet to announce key suppliers, which also need time to ramp up with Tesla's production—signaling further delays in production as well as potential wariness by local suppliers to work with a notably petulant manufacturer already known to pay suppliers late or not at all

There's no guarantee Tesla can make all this happen. In the meantime, it already has irritated Chinese buyers by implementing several rounds of price cuts. Chinese owners of Tesla Model 3s produced locally could get more unpleasant surprises later when Tesla blends its significant manufacturing problems with even less management oversight in Shanghai, escalating already troubling quality and reliability issues which could dampen demand as it's done in the US.

Hint of the last straw

The 10-Q disclosed that Tesla is only now reporting that it amended its factory lease agreement with Panasonic on March 25th. There are many reasons why this is more than interesting, and the first clue is that JB Straubel didn't sign it.

Straubel is the last remaining co-founder of Tesla, after CEO Elon Musk, and he suddenly announced last week he is leaving. Straubel was Chief Technology Officer, described by Bloomberg as "the soul of the automaker—a true believer in electric cars and how they could reshape the world. He has been the quiet, grounded complement to Musk’s drama-filled, visionary persona."

Straubel also was a pioneer that identified and helped adopt lithium-ion battery technology foundational to Tesla's existence. Tesla described his duties as:

JB focuses on technical direction and engineering design including battery technology, power electronics, motors, software, firmware and controls.JB also launched many Tesla initiatives including: the Tesla Energy business providing grid storage for commercial utilities and residential consumers; the worldwide Tesla Supercharger network of fast DC chargers; and the Tesla Gigafactory which is leading the way toward increasing worldwide battery production and lowering the cost per kWh. He also has responsibility for new technology evaluation, R&D and technical diligence review of key vendors.

So as head Battery Guy, Straubel handled Tesla's Panasonic relationship and all things battery related, including the Gigafactory Tesla jointly operates with Panasonic which makes all the battery cells and assembled battery packs used in Model 3. This meant he has signed Tesla's legal agreements with Panasonic for years. Until March.

Right after this latest amendment was signed by a lower level VP instead of Straubel, Panasonic made the stunning announcement in April that it was halting further investment in the Gigafactory it jointly operates with Tesla. Not long before this amendment was signed, Tesla announced it was buying beleaguered Maxwell Technologies.

Maxwell is the long-struggling battery tech maker Musk has tethered to Tesla's future, which now apparently will involve plans to make its own batteries.

I'm not the only skeptic about Maxwell, for a variety of reasons, which is why it was nearly bankrupt again when Tesla bought it. Panasonic and Toyota, for example, have long known about Maxwell's widely promoted "breakthrough" dry battery electrode manufacturing concept since it was announced nearly four years ago. They weren't interested.

Musk began to seriously pursue Maxwell late last fall, about the same time Panasonic was pursuing a collaboration with Toyota to develop more advanced battery technology—as in Tesla was not invited. Indeed, the day immediately after Toyota and Panasonic announced their agreement "to begin studying the feasibility of a joint automotive prismatic battery business,” Tesla expressed formal interest in buying Maxwell. After Toyota and Panasonic expanded their collaboration into a joint venture late in January, Tesla announced on February 4th it was buying Maxwell.

When Tesla began to get serious about Maxwell, Straubel began to sell his Tesla stock. The thing is, he rarely trades his stock at all, and hadn't sold a share since May 2017. However, Straubel started selling his Tesla stock last November with eight transactions overall through June totaling $30 million—approximately a third of his stake.

Buying long-troubled Maxwell is only the beginning of comprehensive and prohibitively expensive complications Tesla will encounter, with no guarantee of success, if it is planning to launch its own battery cell production. For one thing, it's going to need significantly more space and specialized equipment—much like conditions existing at the Gigafactory where it would compete in battery making with Panasonic, for example, it's most important battery cell supplier. Hence, perhaps, the need to amend their Gigafactory lease agreement.

Awkward.

Straubel surely has been through the wringer more than once over the past sixteen years as he worked with Musk to build Tesla into the commanding, albeit chronically troubled market player it is today. That's over now. Whatever Musk has planned for Tesla's future battery and other technology endeavors, Straubel wants no part of it.

And that is alarming.

TSLA 5.3% Senior Notes due 2025 are little changed since my last report at 87.9 (7.9% ytw; 602 bps). That’s a measly 88 bps of spread per turn of estimated leverage by yearend 2019, woefully inadequate compensation for such a volatile issuer with such precarious prospects. Given Tesla's persistent uncertainty and escalating risks, there's a good risk of 3-5 points of downside from here. Maintain “Underperform."

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.