Musk and Weird Q3 Developments Are Driving Investors to Telsa's Rivals

Brings to mind Bob Dylan's "there must be some kind of way out of here, said the joker to the thief."

Baillie Gifford & Co., 3rd largest investor in Tesla Motors (TSLA US) with a 7.7% stake, reported after the market closed on Tuesday that it has taken an 11.4% stake in Tesla rival, Shanghai-based NIO Inc.Ballie's $515 million investment (85.3 million shares) amounts to more than half the $1 billion NIO just raised in its US IPO last month.

Credit embattled CEO Elon Musk's arrogantly irresponsible behavior for alarming Tesla's investors so much that even dicey NIO looks like a better home for fresh cash by comparison.

Musk has demonstrated he can't be trusted during yet another problematic quarter for Tesla, just as investors struggle to gauge Tesla's underlying operating performance and financial condition versus what Musk has described and projected.

"There must be some kind of way out of here, said the joker to the thief."

Bob Dylan

The beginning of the end for renowned inventor Nikola Tesla came when he lost the faith of his investors, including the venerable J.P. Morgan.

For all his brilliance, Tesla also was prickly and arrogant--much like Musk. Similarly, Tesla was particularly contemptuous of contemporaries Thomas Edison and George Westinghouse, believing his own intellect as unequivocally superior by comparison.

Yet Edison and Westinghouse built enduring empires versus Tesla, who died bitter and penniless because, as it turned out, he was a terrible businessman.

It wasn't Tesla's haughtiness that drove away his investors, it was his failure to execute as promised.

Musk has made it increasingly difficult for investors

His wildly exaggerated projections have turned into dramatic shortfalls in Tesla's operating performance and earnings versus guidance, capped by his irrational and even destructive behavior. Indeed the Saudi Arabia Public Investment Fund, which featured prominently in the "funding secured" part of Musk's debunked buyout scheme in early August, curtailed its investment plans with Tesla after the initial $2 billion (near 5% stake) it purchased in Tesla stock around July, apparently put off by Musk's outrageous stunt and the unseemly publicity it created.

Saudi PIF instead directed a subsequent $1 billion into Tesla's rival Lucid, with Saudi Crown Prince Mohammed Bin Salman saying last week Tesla's are "nice" but he didn't want to own one any time soon.

Then Baillie Gifford & Co., top investor in Tesla with a 7.7% stake, reported after the market closed on Tuesday that it has taken an 11.4% stake in Tesla rival, Shanghai-based NIO Inc.Ballie's $515 million investment (85.3 million shares) amounts to more than half the $1 billion NIO just raised in its US IPO last month, and it's also nearly twice what Tesla needs to pay off in maturing debt due in November.

Credit Musk for alarming Tesla's investors so much that even dicey NIO and Lucid look like a better home for a sizable chunk of fresh cash by comparison.

On Wednesday, T. Rowe Price reported it had increased its stake in Tesla to 10.2% as of the end of September, nudging it above Ballie as the top outside investor after Musk.

This failed to offset the wave of negative news, however, plus Price essentially was buying back at Tesla's much lower stock price much of what it sold off in the June quarter.

It hasn't helped that Musk's buyout debacle triggered an SEC investigation into securities fraud along with a similar criminal investigation by the Department of Justice and numerous shareholder lawsuits.

Or that Musk immediately insulted the SEC after the agency gave him a decidedly favorable settlement deal, which even now is being evaluated by a skeptical federal judge in the Southern District of New York (see my reports "Tesla: Looking for Trouble" and Telsa Party Today; Hang the Details" and "What Tesla Can Learn From Navistar About Arrogant Management, Serious Mistakes, and Survival").

Actions have consequences, and Musk has so unnerved investors that Tesla has lost more than $20 billion in evaporated market cap in just the past couple of months, and created likely years of escalating legal troubles for Tesla that are costly to defend and will be even more expensive to resolve.

Tesla’s 5.3% senior notes were substantially oversubscribed when they were issued just a year ago in August—hence the cheap coupon considering the initial "B3/B-" credit quality ratings assigned by Moody's and Standard & Poor's (now Caa1/B-). They have been in decline ever since and were last seen trading near 83.8 (8.5% ytw; 530 bps).

The cost to hedge Tesla's debt against default using credit default swaps has hovered near highs for more than a month and was last seen at 21.7%--$2.17 million to insure $10 million in Tesla bonds.

The thrill is gone; what's next?

As Musk destroys Tesla's mystique, investors now mostly brace for what might come next:

It remains to be seen how well Musk and Tesla fare under court-mandated management oversight by Tesla's feckless and insular board, especially after Musk steps down as Chairman as directed within 45 days.

I doubt this will stop Musk from being Musk, especially if he gets to hand-pick a buddy as his successor (see my concerns that the SEC's remedies don't go far enough to address serious management deficiencies, along with my suggested list of fixes here).

Tesla will report third-quarter results by the end of October, and actual underlying operating performance and financial condition could vary broadly versus what Musk has described and projected. Unfortunately, Musk has demonstrated during yet another problematic quarter for Tesla that he can't be trusted.

It started out ok, but then...

Musk's has projected positive GAAP profitability and free cash flow--for the first time--for both quarters in the second half of the year, with sequentially improving gross margin for Model 3 of 15% and 18%, respectively.

Model 3 deliveries are projected to exceed targeted production of 50,000-55,000 for the third quarter, with Model S and X deliveries projected to accelerate through the end of the year, distributed more smoothly throughout each quarter versus the typical pileup at quarter-end, and totaling 100,000 for the year.

Cash flow was projected as sufficient to cover cash obligations, including debt due through yearend. This seemed ambitious since it implies a positive swing by more than $2 billion sequentially versus the first half of this year and compared with the second half of last year.

Last week Tesla announced seemingly good news about sales in the third quarter, with total deliveries of 83,500 including 55,840 in Model 3. Deliveries of higher priced/higher margin Models S and X were up a tepid 1.3% y/y, and guidance was maintained.

That might be a stretch since deliveries of both models actually were very lumpy throughout the quarter and included falling US sales of Model S and falling sales of Model X outside the US—as I projected.

Tesla med guidance for positive income and free cash flow, which seems even more ambitious now given the myriad of unexpected (read more costly than expected) problems. Telsa also failed to update or confirm Model 3 order count as has been typical, versus the previously reported 420,000 at the end of the second quarter.

This is concerning because Musk never seems to miss an opportunity to crow if the news is good (true or not).

Toss in the Disturbing, Weird, and Maybe Not Even True

July 16 - Musk calls the British diver helping with the Thai cave rescue a pedophile; continues taunting until the diver sues him 2 months later.

August 7 - Musk tweets out his ill-advised, unsupported, and thoroughly misrepresented buyout plan which immediately crumbles under scrutiny and is abandoned 3 weeks later--triggering federal investigations and numerous shareholder lawsuits citing fraud. The SEC begins investigating Musk for securities fraud the next day. I suggested his stunt may have been a desperate move to deflect his increasing concern that the critically important third quarter, then about half over, was not going well.

August 16 - Tesla maintains it can't produce enough cars to meet unsatiated demand yet it reportedly started sending line workers home well shy of weekly production targets--suggesting either demand actually is fading or Tesla may have been forced to cut costs to preserve cash--or both. Tesla also said around this time it voluntarily paid down $500 million in revolver debt--that wasn't due--which made me wonder if Tesla's banks are getting worried.

August 16 - Speaking of more to worry about, the Wall Street Journal reported the SEC is investigating whether Musk made false statements related to problems with Model 3 production in 2017 when Tesla raised billions in cash selling stock and bonds. As it turned out, Tesla produced only 2,700 Model 3s versus his projected production guidance which ranged from 200,000 (made in mid-2016) to 20,000 (made in mid-2017).

August 17 - Musk gave a disastrously emotional interview with the New York Times, followed by a desperate tweet to Arianna Huffington declaring he must spend day and night at the factory to keep Tesla from bankruptcy (later it's revealed he probably wasn't spending day and night at the factory).

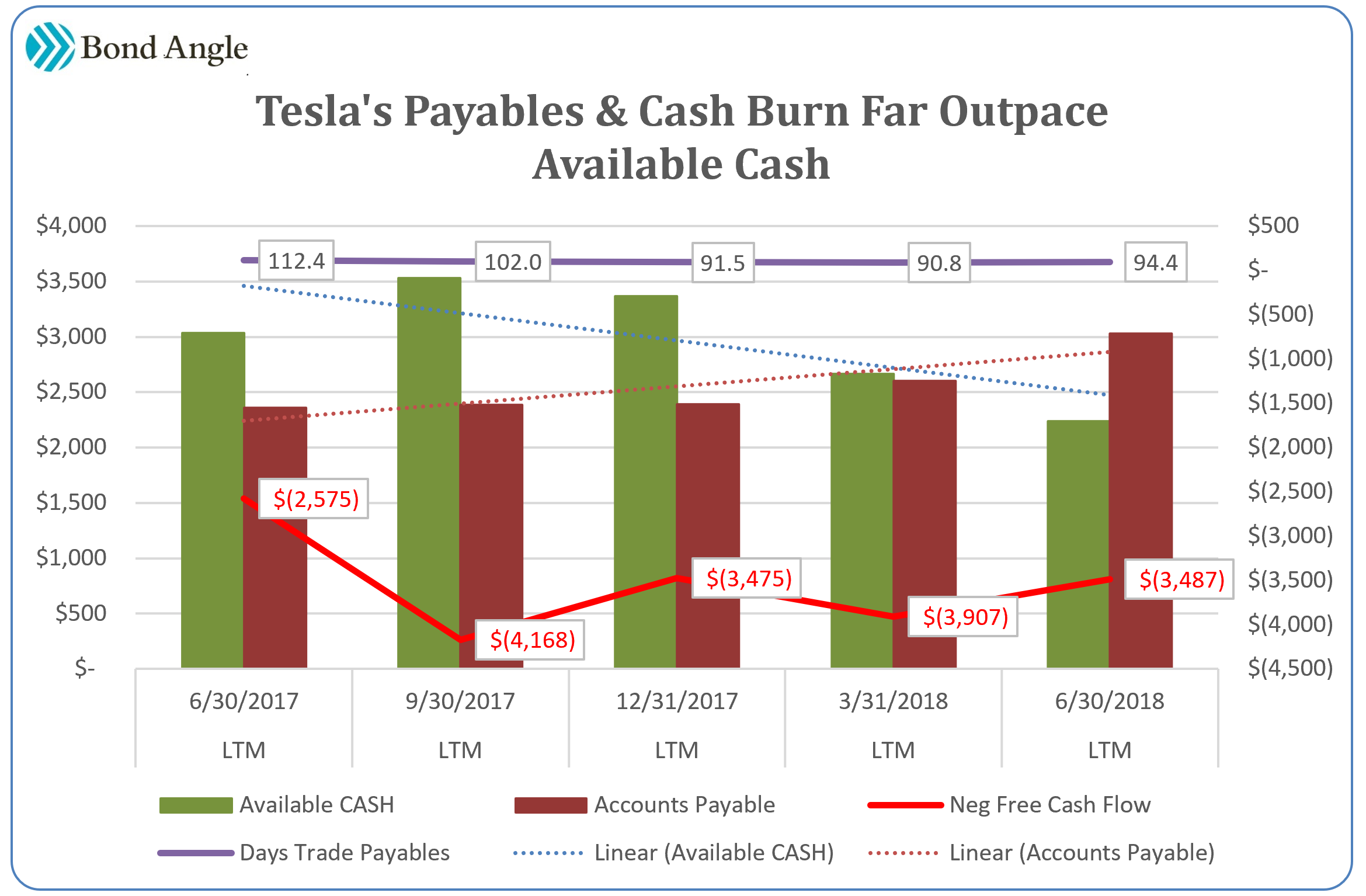

August 20 - The Wall Street Journal reported that Tesla seems to have serious problems making timely payments to vendors--and they can shut it down if they don't get paid. This calls into question Tesla's confident guidance of positive and accelerating cash flow it claims it can even boost further by reducing capex.

This concern is bolstered by the troubling exit during the quarter of several key Accounting, Finance, and Supply Chain executives, which I have warned signals liquidity pressure plus potential "irregularities" that may surface later with accounting, compliance, and management oversight when yearend financial statements are produced and audited.

August 21 - Business Insider revealed that 71% of the Model 3s Tesla rammed through production to meet the 5,000 production goal the last week of the June quarter had such serious defects they had to be reworked.

Other evidence surfaced which persisted through the quarter that Tesla also is delivering defective cars to customers, revealing continuing production chaos plus failing quality controls and increasingly dismal customer service.

Of course, Musk knew about these problems on August 1st when second-quarter results were reported and he was boasting that Tesla had made such great strides with production that costs were falling on accelerating output.

Tesla also fell well short of production targets for 7,000 per week in the third quarter, though it employed a similarly desperate fire drill with deliveries at quarter-end.

September 7 - Musk smokes marijuana during a live show, following another round of key management departures. Tesla stock wipes out 5 months of gains in a day when the price dropped to $263. It later dropped to $250 on October 8th, the lowest since March 2017.

September 9 - After all Musk's complaining about "production hell" Tesla suddenly has sufficient surplus Model 3s available that it begins to offer special sales events, including "first come, first serve" sales where buyers can pick up cars almost immediately.

I suggested this implies potentially rising cancellation rates, concerns not helped by Tesla's failure to update Model 3 order count and a potential threat to fourth quarter unit sales and average pricing.

I also warned about potentially fading demand as implied by stories which continue to surface about hundreds of new, apparently unsold cars parked in lots all over the country, and which recently also caught the attention of the New York Times.

September 14 - Large numbers of mysteriously parked cars plus the sudden and surprising availability of cars for immediate sale clashes with claims by the company of months in unsatiated demand. Indeed tabulations of reported production totals versus delivery totals don't seem to align, even given Tesla's reports of cars "in transit" at quarter-end. What's going on with inventory and deliveries?

This seems even more disturbing given increasing stories of buyers paying cash up front but still waiting weeks for their cars. Add to this stories about delivery dates abruptly broken, restarting the wait, and of buyers that were promised specific cars--with VINs assigned--which were given to other buyers.

This could be further incompetence, of which Tesla has shown plenty, but it also could be a maneuver to reap sorely needed cash and even double-book revenue--a worrisome concern not helped by the troubling exodus of so many senior accounting and finance executives also occurring during the quarter.

September 18 - Bloomberg reported the Department of Justice had launched a criminal investigation into Musk's actions and public statements related to his buyout debacle.

September 24 - Musk blames an "extreme shortage" car carriers for potentially delayed deliveries to customers, tweeting Tesla was forced to start "building our own car carriers this weekend to alleviate load." His claim was immediately disputed by trucking industry leaders who reported there actually were plenty of carriers and drivers available. This was supported by Twitter sleuths, who took numerous pictures of empty carriers in and around Tesla facilities through quarter-end.

September 27 - The SEC sues Musk for securities fraudand seeks to bar him from serving as an officer or director of a public company. Musk settles two days later; afterward, it's also revealed that he had petulantly walked away from the remarkably benign first settlement deal offered to him which he already had accepted.

Musk then immediately insulted the SEC in a tweet, just before the settlement terms were due to be submitted for federal court approval. The judge sent Musk and Tesla and the SEC home to compile a letter that was submitted this week explaining why the SEC's recommendations comprise sufficient penalties for Musk's actions and behavior versus the harm caused (hint: no, they don't).

September 28 - The final business day of the quarter was marked by the filing of an amended whistleblower lawsuit, Wochos v. Tesla, which bolsters serious questions raised about Model 3 production in 2017 by The Wall Street Journal and the ongoing SEC investigation with statements from now 12 different former Tesla employees.

September 30 - Musk says in an email to employees that Tesla is "very close" to profitability for Q3 but still needs a big push on last day of the quarter to make it happen. "Very Close" means not profitable just like an email to employees does not mean appropriate public disclosure necessary when Tesla's CEO signals potentially yet another miss in quarterly guidance (as I have projected).

So ends another Tesla-style quarter.

There's little reason to believe anything to be true about third-quarter results or what Musk says about third-quarter results until we see the formal press release; even better, wait for the10-Q.

There is plenty to be wary about, including notable evidence of higher than expected costs as indicated by general chaos and inefficiency persisting throughout the quarter, plus signs of potentially weaker than expected revenue given possibly significant pricing pressure from fading solar credit subsidies, China tariffs, weaker mix, and surprising special sales events deemed necessary to move inventory quickly.

If so, Tesla also is likely to burn through more cash than expected, pressuring already tight liquidity ahead of hefty debt maturities over the next year--necessitating a near-term action plan such as refinancing transactions I have recommended.

I remain concerned that Tesla will fall short of management's guidance and market estimates for third-quarter results, as published in my latest model.

Maintain “Underperform” on TSLA 5.3% Senior Notes due 2025, down nearly 3 points over the past week to 83.8 (8.5% ytw; 530 bps), approaching the 82.9 low hit last month. Given Tesla's persistently volatile situation we still could see 3-5 points additional downside from here.

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.