SoftBank Who? WeWork Picks Bank Bailout; Bondholders Beware

WeWork rejects rescue plan from SoftBank, its largest investor and most stalwart patron, in favor of a truly hideous "bailout" package from its banks. Gee, what could go wrong?

Bloomberg reported overnight that The We Company (WeWork) (WE US) has rejected the buyout plan proposed by SoftBank Corp (9434 JP), its largest investor and biggest backer (see my report last night SoftBank May Blink First (WeWork Bondholders Hope).

WeWork has chosen instead to go with the bailout plan proposed by its Banks which calls for adding massive layers of expensive unsecured, likely unregistered debt to its balance sheet--along with dramatically reduced exposure for the banks with plenty of coverage (at pricey fees, no doubt) to protect them from WeWork's alarming and escalating risk.

Gee, how bad could it be?

For starters, PIK notes. Billions in PIK notes...

Sit Down, SoftBank

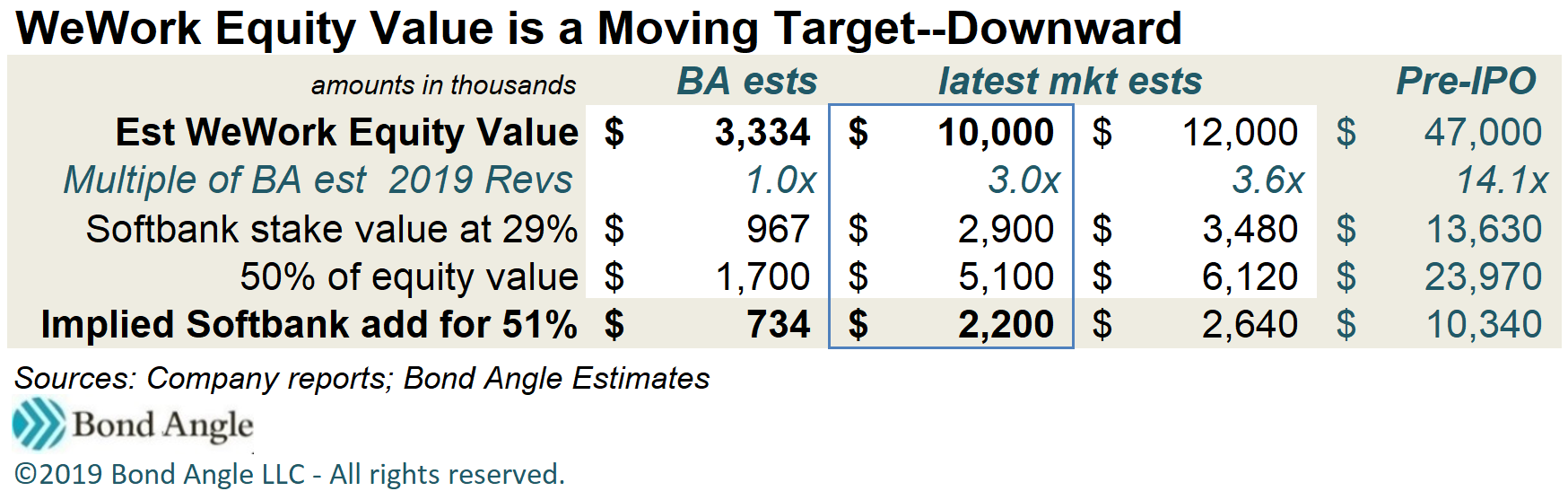

I detailed in last night's report SoftBank's plan to buy out a controlling interest in WeWork which, given the dramatic collapse in equity value, could be done at something between $2.2-2.6 billion.

For SoftBank, WeWork's catastrophic collapse already has resulted in a sickening write-down of its $11 billion investment by at least 75-80%, assuming the $10-12 billion equity valuations floated last month (my estimate is $3 billion, which probably is generous given the company is on the verge of bankruptcy).

However, buying a controlling interest would enable SoftBank to better participate in WeWork's urgent recovery on the road to retracing its prohibitive losses.

For WeWork SoftBank represents a stalwart, deep-pockets patron as well as investor, with years of demonstrated financial support from billions in equity injections and loans which we now know have been vital to keeping the company afloat as long as it has (see Gravity Works As WeWork Doesn't; Now Plan B).

Importantly, SoftBank also supported WeWork's management autonomy, even after years of the company's failures to deliver on its perpetually overambitious promises while Adam Neumann was at the helm. While this raised concerns for investors in WeWork and SoftBank, WeWork's new, more credible co-management, could likely rely on SoftBank's continued support of their turnaround plans.

SoftBank's strong financial support as a committed owner with ample financial capacity also could represent the most important ammunition WeWork can muster in helping to restore its shredded credibility, enabling it to proceed with restructuring its business model and sign deals with counterparties who can trust it.

As I noted in The Tide Is Out and WeWork Bondholders Are Naked:

Just weeks ago WeWork still was being celebrated as the largest and fastest-growing tenant for commercial office space in some of the most important cities worldwide, including New York City, Chicago, Dublin, and London, aiming for an astonishing $3 trillion in global revenue opportunities as of its S-1 filing.

Now WeWork has become a bright red flag in those markets with current and prospective customers and landlords scrambling to assess its viability going forward.

WeWork's new joint-CEOs, as their first order of business last week, terminated current negotiations with landlords for new lease agreements and sharply curtailed others to preserve cash.

New business WeWork was expected to get is being snapped up by rivals, which also are taking calls from WeWork landlords about potentially taking over if the company fails. Other deals have fallen apart because counterparties are wary about signing up business WeWork potentially can't afford to execute.

WeWork's bondholders would benefit substantially from WeWork owned by a large, well-capitalized parent, which could ease some perpetual detractions that impair bond value such as being unregistered and hard to trade with little if any market coverage.

Even without liquid trading and convincingly accurate market pricing or sound financial information, transparency, and public reporting, it's much more relaxing to be able to clip the coupon you know is probably coming on bonds that probably will be repaid upon maturity in 2025.

But, apparently, WeWork's management and feckless board--which rubber-stamped every move Adam Neumann made--considered the obvious advantages of SoftBank's plan as less important now, as they struggle to save the company, versus retaining their absolute power by keeping the company independent, such as it is.

This means aligning with WeWork's Banks which have demonstrated they will not be there to backstop the company when it becomes distressed--they bolster own their risk coverage instead.

Ego, Control Win the Day

WeWork chose instead the bailout proposed by its legacy banks, even though it's long been clear they are clearly have been increasingly wary about the company's escalating risk and shattered prospects (see Gravity Works As WeWork Doesn't; Now Plan B).

This is not to be confused with opportunities the banks embraced in pursuit of hundreds of millions in fees they could generate by selling the company's securities; e.g. JPMorgan Chase & Co (JPM US), Goldman Sachs Group (GS US), and Morgan Stanley (MS US) pitched WeWork to investors last year at $50-100 billion and fought each other over leading its IPO when it was valued at $47 billion.

JPMorgan, Goldman, Morgan Stanley, and other core WeWork banks also ran the WeWork's high yield bond offering in April 2018, also supported with a woefully inadequate prospectus, during a quarter when the company's operating margins turned out to be shrinking rapidly with losses mounting alarmingly which wasn't revealed until long after the bonds were sold and trading below par.

So if hundreds of millions in fees could be reaped, WeWork banks are all in. But when it comes to their own exposure, not so much.

From SoftBank May Blink First (WeWork Bondholders Hope):

But when it was time to bring the IPO to market, the $6 billion in credit facilities they arranged were priced with steep terms and shorter maturities and set to close only if the IPO closed.

Some $2 billion of that total amount comprised a Letter of Credit facility which charged interest and required WeWork to provide 100% collateral in cash--a clear sign to me at the time of the banks' wary view of WeWork's disturbing credit risk.

The only thing that has changed since August, despite likely two months or more of negotiations, is that the banks are willing to lend even less.

I have observed for months that WeWork's banks have been adamant about not moving forward with closing new credit facilities which will provide sorely needed liquidity. Remember, banks get much more comprehensive financial information about WeWork than typical investors, and they get it every month.

So I have been very concerned that the banks have consistently moved to reduce their own exposure by slashing their credit commitments, casting off risk to other securities, like a massive $3 billion chunk of unsecured high yield notes, and seemingly requiring SoftBank to contribute additional equity before they would agree to greatly reduced credit facilities.

This is glaringly obvious in the bank's bailout package which WeWork accepted.

As it turns out, that $3 billion offering in high yield debt is to include "at least $2 billion of unsecured payment-in-kind notes with an unusually hefty 15% coupon," according to Bloomberg. That's nearly 3x more versus the $669 million currently outstanding in WeWork's unregistered 7.875% notes due 2025.

Payment-in-kind notes mean coupon payments are paid in more bonds instead of cash. Such notes are rare because they typically are highly undesirable since they are issued by extremely distressed companies and end up adding to an already massive debt load they company struggles to support.

Think even 15% is high enough to accommodate risk sufficiently to satisfy prospective investors? Nope, and not even the banks think so, as Bloomberg reports:

The $2 billion of proposed unsecured debt may carry an additional sweetener for investors: equity warrants designed so that investors could boost their return to around 30% if the company gets to a $20 billion valuation, according to the person who described the structure. WeWork would pay only a third of the coupon in cash, while the rest of the interest would accumulate and become due at maturity, the person said.

So investors will be offered unregistered bonds that pay only 30% of their coupon in cash while piling on more debt plus get warrants to potentially redeem years down the road when WeWork--a nonpublic company--may claim to be worth $20 billion in equity value based on demonstrably flawed, oblique, and misleading financial statements. The banks value this issue at 15% yield plus warrants--I suggest at least 18% yield for a likely 5-7 year maturity as more appropriate for investors to accept.

After all, WeWork's credit metrics remain off the chart ugly with GAAP EBITDA at -$2 billion for LTM as of June 30th on just $2.6 billion in revenue--I expect modest improvement at best over the next two years.

Yet just two months ago the "smart money" still valued WeWork at $47 billion. The same banks selling these notes, and that sold the WeWork bonds in April 2018 which traded recently at 12% ytw, pitched the company as being worth $50-100 billion last year before it reported a stunning loss at $1.9 billion for 2018 which so far have been topped by worse losses this year with $2.1 billion for LTM as of June 30th.

At the very least prospective investors in WeWork's new bonds should demand that the company file SEC quality financial statements and distribute them to Holders, Prospective Holders, and Securities Analysts to facilitate better transparency in financial reporting, trading, and market pricing. Even better, avoid them altogether.

That's not all. The $2 billion in PIK notes will be joined by another $1 billion in secured debt, likely high yield notes. I am skeptical of the quality and value of assets offered as collateral to back these notes since WeWork has a comparatively modest proportion of credibly tangible assets and asset value reported on the balance sheet is likely overstated. I expect these notes also to be priced too low--I suggest at least 12-15% yield depending on maturity and collateral offered.

Moreover, I also have noted, WeWork's banks will ensure they are most comfortably covered by the best claims to the best assets, and that will limit coverage available for the bonds as well as what the banks actually will lend in credit facilities.

Sure enough, the only other piece left in the proposed package is $1.7 billion for a letter of credit facility "split among participating banks."

Presumably, terms will be similar to the previous LoC facility arranged back in August before the IPO was filed when everyone still loved WeWork. Even then the banks planned to require WeWork to back every draw on the LoC facility with 100% cash collateral--plus interest at L+100 bps.

That's it--$4.7 billion in total new debt comprising a $1.7 billion LoC facility plus a whopping $3 billion in pricey high yield debt. The banks have completely eliminated the term loan commitment previously offered which had comprised $4 billion, priced at L+475 bps, of the total $6 billion they had arranged back in August.

So the banks not only intend to lend less, they really aren't lending any more at all, since the LoC facility will likely be collateralized if drawn with 100% in WeWork cash. This leaves WeWork with its existing $650 million revolver, which had only $350 million in available credit as of June 30th.

In the meantime, SoftBank apparently is not on board with this plan and so is not kicking in the extra $1 billion in new equity it had offered since August. That means no new cash from SoftBank until the $1.5 billion it had pledged to invest next year.

So in the first test of WeWork's new management's decision prowess and focus, it turned away the company's most important patron, SoftBank, which also could have fast-tracked the restoration of the company's business reputation and prospects while likely ensuring strong and continuing financial support to help fund the multi-year turnaround ahead. This would have eased concerns for all of WeWork's worried stakeholders, but it also meant yielding control in the meantime until SoftBank elected to spin it off again down the road. Oh the horror.

Instead, WeWork accepted a large, terribly expensive debt package that will further burden its bloodied balance sheet, fail to eliminate its liquidity pressure for long, and fail to restore confidence in the company's long-term viability.

WeWork needed to raise $9-10 billion in stock and debt back in August when it was the darling of Wall Street, and I have estimated it could run through that cash in a year. Now as it faces its most distressing business and financial challenges of its existence, it will be lucky to net less than $5 billion in fresh funds while taking on an even more overburdened balance sheet.

Good talk guys.

Bondholders, I recommend again to use any rally as an escape pod.

WeWork 7.875% senior notes have rallied 7 points to 90.5 (10.2% ytw/860 bps) since my last report. WeWork remains severely distressed and it's not yet clear whether the company can remain viable for the foreseeable future. Existing bonds face the further risk of the company's pending note offerings which will envelop them in a mountain of debt without providing a convincing path for the company's recovery. Upside potential remains limited outside of brief, misguided rallies as a result while downside risk could be 5-10 points from here over the near term. Maintain “Sell.”

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.