WeWork Bondholders Brace for SoftBank’s Rescue Plan—In Silence

As expected, WeWork bondholders are still in the dark about when SoftBank will start its rescue plan (burying bonds with billions of new debt) or even if it's been approved by shareholders. SoftBank i

As I expected, The We Company (WeWork) (WE US) has gone silent (see The Tide Is Out and WeWork Bondholders Are Naked).

Given the urgency of WeWork's financial distress, it is worrisome that further details about massive new debt coming as part of the SoftBank Group (ADR) (SFTBY US) rescue plan announced last week have yet to be publicized. Get used to it.

As I warned again in SoftBank May Blink First (WeWork Bondholders Hope), WeWork "will not change its practice of providing bondholders inadequate information which then fails to reflect the company's true and accurate financial condition and prospects--because it's not required to" since it pulled its IPO and is no longer subject to any SEC-required financial reporting standards.

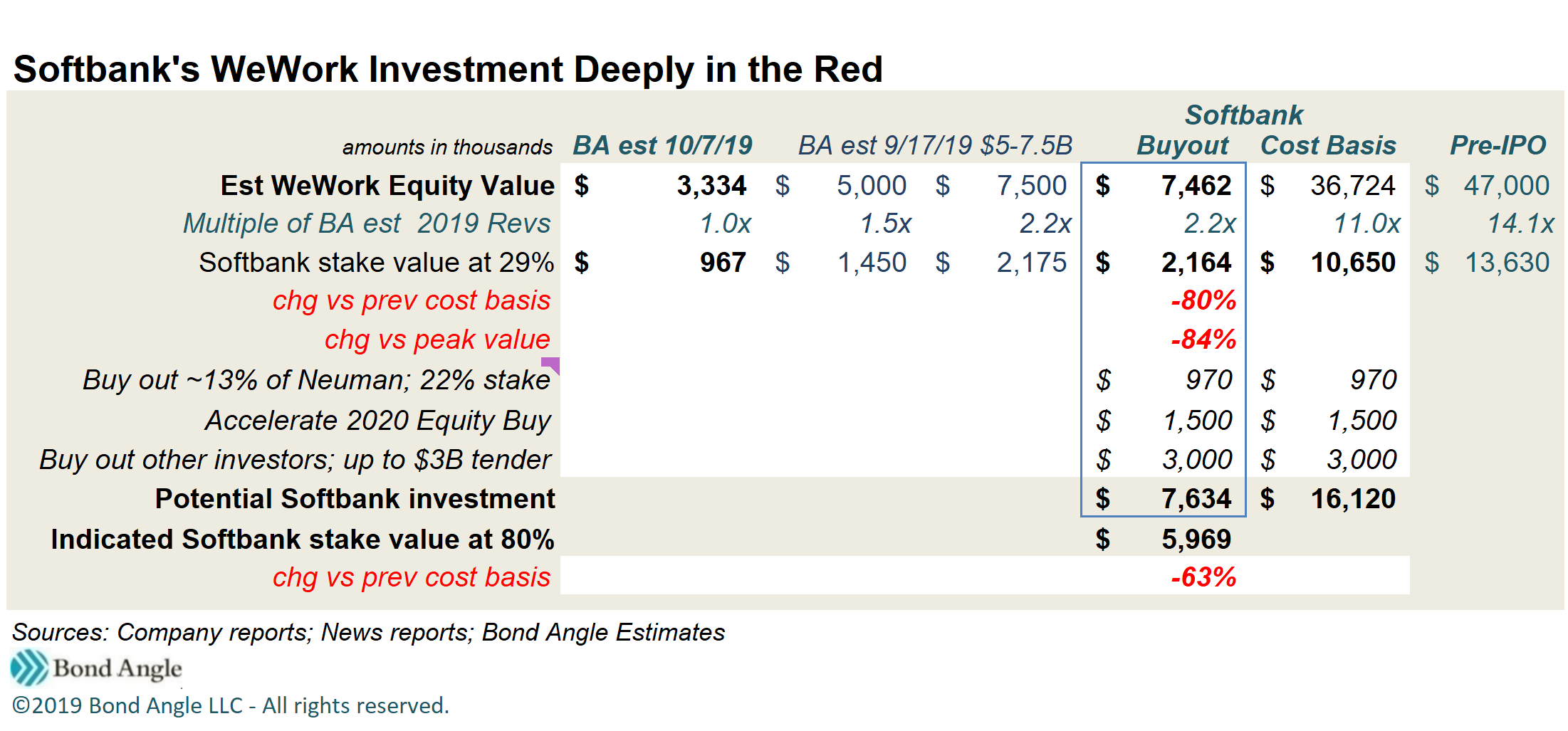

WeWork now is valued near $7 billion—well within the $5-7.5 billion range I projected in mid-September in Gravity Works As WeWork Doesn't; Now Plan B, which now still seems generous since the company is on the brink of bankruptcy.

I thought as much by October when I cut my number to roughly $3 billion, affirming my previous estimate that the company has much less cash than advertised and thus could run out by yearend (The Tide Is Out and WeWork Bondholders Are Naked). This also was subsequently confirmed.

It's not just that WeWork needs literally billions in emergency cash right now to stay afloat, it's also that it likely will need such expensive financial support for the foreseeable future.

That troubles SoftBank's stock and bondholders who worry about throwing billions more into what could be SoftBank’s worst investment ever.

This should alarm WeWork bondholders as well.

About That Fine Print

I have been warning for weeks that investors need to read the fine print in any confirmed deal to rescue WeWork, and here it is: SoftBank is not *acquiring* WeWork; it will not take *control* of WeWork.

Terms of the deal were engineered to avoid change-of-control so SoftBank will not consolidate WeWork into its operations or financial statements, as detailed in last week's press release announcing the news which was signed by WeWork's newly minted Executive Chairman Marcelo Claure, already installed by SoftBank:

"After closing, and following the tender offer, SoftBank’s fully diluted economic ownership of WeWork will be approximately 80 percent. Since SoftBank will not hold a majority of voting rights at any general stockholder meeting or board of directors (“Board”) meeting and does not control the Company, WeWork will not be a subsidiary of SoftBank. WeWork will be an associate of SoftBank."

This obviously saves SoftBank from staining its own financial statements with WeWork's multi-billion dollar losses and its massive debt and lease obligations, including $47 billion in expensive long term leases that swamp its modest annual revenue which I have estimated at roughly $3.3 billion for 2019 with little if any improvement next year (see Gravity Works As WeWork Doesn't; Now Plan B and subsequent reports). It doesn't erase the damage SoftBank's WeWork investment already has done to its portfolio.

SoftBank has sunk more than $11 billion in equity and loans into WeWork since it first invested $4.4 billion just two years ago, which boosted the company's value from $16.9 billion to $20 billion.

With the rescue plan, SoftBank's investment jumps immediately with another $1.5 billion equity injection before buying out ex-CEO Adam Neumann's stake for $970 million (plus $500 million to pay off Neumann's loans from JPMorgan backed by WeWork stock) and as much as $3 billion spent to tender stock from other investors.

Now SoftBank values equity in this sinking ship as worth closer to $7 billion, finally in-line with my pre-IPO estimate but still more than twice my current number. Either way, the value trails $47 billion where its last invested in January this year, marking a massive loss for SoftBank and its Vision Fund which already has scared investors away from Vision Fund II which it's trying to sell now.

And yet, as I noted in SoftBank May Blink First (WeWork Bondholders Hope), SoftBank had few options but to salvage its grossly inflated investment; all ugly:

One item that didn't appear in any of the WeWork brochures was that it was mere months from bankruptcy if it failed to raise $9-10 billion from its IPO and new credit facilities arranged back in August. But there were plenty of clues.

For one, WeWork's cash consumption is voracious and unrelenting--much like its mounting losses which continue to outrun even rapid revenue growth which now is threatened by the recent revelations of its dramatically inflated profitability, prospects, and value.

As I noted again in The Tide Is Out and WeWork Bondholders Are Naked, WeWork burned through $6-8 billion in cash during 2018 through June 2019, including all the substantial cash raised from borrowing and equity infusions. This compared to revenue at just $1.8 billion for 2018 and $2.6 billion generated for the LTM ended June 30, 2019. It lost $1.9 billion and $2.1 billion, respectively, over those same periods.

I estimated that WeWork "was set to consume all the $9-10 billion it planned to raise in stock and debt in a year or less with still no convincing path to profits or positive free cash flow."

I also noted that WeWork's effective available cash was much lower than reported at $1.4 billion as of June 30th, and this could be depleted by yearend.

Meanwhile, WeWork failed miserably at attracting new investment elsewhere. A "leaked" email from its new co-CEOs (potentially soon to be replaced by SoftBank) shows WeWork approached 75 additional funding sources--apparently none were interested in terms offered.

It's little wonder since multiple sources since early reports now confirm WeWork has burned through most if not all the $1.4 billion I calculated as actually available cash as of June 30th versus $2.5 billion reported (see Gravity Works As WeWork Doesn't; Now Plan B) as I expected, and likely the nominal $350 million it had reported in available credit on its $650 million revolver. Given its accelerating distress, I had estimated that WeWork could be burning through $2-3 billion per quarter and its turnaround, if it happens, could take 2-3 years.

Recent reports say even SoftBank thinks the turnaround could take three years as it shifts WeWork's focus to slower, more conservatively targeted revenue growth in core operations and key markets plus stringent cost management.

WeWork's Banks Have Been Looking For Cover

I was not surprised that WeWork's JPMorgan Chase & Co (JPM US)-led legacy banks, which had arranged $6 billion in expensive new credit facilities just before the IPO was announced, and which had pitched the company to investors last year as worth $60-100 billion, now refuse to lend it one penny more.

This seemed obvious to me after weeks and then months of foot-dragging passed with no new credit facilities signed long after the IPO was clearly in trouble and then withdrawn.

Instead, the banks were happy to cast off their WeWork risk by selling a bailout package of ugly new, and of course, unregistered bonds to investors (SoftBank Who? WeWork Picks Bank Bailout; Bondholders Beware) with coupons woefully inadequate to compensate for WeWork's horrific and escalating credit risk, as they did in April last year, confirming my suspicion that the banks were seeking to reduce their exposure to WeWork (Gravity Works As WeWork Doesn't; Now Plan B and SoftBank May Blink First (WeWork Bondholders Hope)).

The JPMorgan $5 billion all-debt bailout, which WeWork's board first accepted before being shamed by investor outrage into dropping, included "at least" $2 billion in PIK notes offered at a laughably low 15%yield plus $1 billion in secured notes dubiously backed by questionable asset quality given the overstated book value of WeWork's comparatively minimal tangible assets (see SoftBank Who? WeWork Picks Bank Bailout; Bondholders Beware). WeWork's banks likely have claimed all credible tangible asset value plus a comfortable cushion to account for the company's alarming deterioration, to back its current secured credit facilities.

As I called out in my last report, JPMorgan did not offer a new revolving credit line or term loan in its $5 billion bailout package. Instead, terms included a $1.7 billion letter of credit facility which would be as widely syndicated as possible among multiple banks and, I suspect, likely require 100% cash collateral from WeWork to be posted for every penny drawn plus interest--just like the letter of credit facility the banks arranged back in August.

Here Comes the Son

This left SoftBank to carry the full load for WeWork's bailout, while JPMorgan will still get a $50 million payment for arranging the hideous $5 billion debt package not selected.

SoftBank's takeover package will inject $4.8 billion in cash into WeWork, also mostly from new high yield notes--though no mention of PIK notes:

Existing Payment Obligation: Acceleration of SoftBank’s April 2020 $1.5 billion payment obligation at $11.60 per share, expected to be completed 7 days post-signing, subject to WeWork shareholder approval;

Tender Offer: The launch of a tender offer worth up to $3 billion to all non-SoftBank shareholders at a price of $19.19 per share, expected to commence in the fourth quarter of 2019, with closing subject to regulatory approvals and other customary closing conditions;

New Debt: Consisting of $1.1 billion in Senior Secured Notes, $2.2 billion in Unsecured Notes, and a $1.75 billion Letter of Credit Facility. This funding is expected to occur after the completion of the tender offer; and

Joint Venture Share Swap: All of SoftBank Vision Fund’s interests in regional JVs outside of the Japan JV will be exchanged for shares in WeWork at $11.60 per share.

WeWork Board Press Release, 10/22/19

Note that these terms are subject to shareholder approval. Has this happened? We may presume so given WeWork's cash crisis, but there's been no announcement more than a week later.

There's also been no news about the timing of the bond sales, which also should be coming soon with terms reportedly "better" versus the bonds JPMorgan had proposed. Better for whom is not clear.

It's anyone's guess how long this fresh cash will last, but I suspect WeWork may deplete it faster than expected--perhaps in less than two quarters. After all, this is half what the company was hoping to raise in stock and debt with the IPO--and I had estimated this funding could be depleted in a year or so and WeWork's financial condition and prospects have deteriorated rapidly since then.

In any case, once SoftBank starts writing checks to support WeWork, it may not be able to stop for years.

Massive layoffs have been announced, with likely more to come, along with asset sales of dubiously valued noncore and likely unprofitable businesses like Managed by Q, Meetup, Conductor, SpaceIQ, and Teem. Neither efforts are likely to move the needle sufficiently to staunch WeWork's accelerating losses and cash consumption (see WeWork Board to CEO: YouOUT and The Tide Is Out and WeWork Bondholders Are Naked). SoftBank also is expected to throw business WeWork's way and have it refurbish SoftBank offices.

These measures won't be enough to stabilize WeWork's foundering operations, worsened by tumbling revenue as it's being forced to scale back on new and existing business in lucrative--and expensive--markets like London, New York, China, parts of Asia, and Latin America.

Neither will this offset WeWork's biggest margin squeeze: rent, which is its largest and least flexible expense. I have estimated rent expense in 2019 could claim 76% of revenue at $2.5 billion, a number already increasing into next year on deals signed through at least August. This could grow to more than $10 billion over the next four years, according to WeWork's S-1 filing.

Leases also can deplete cash if WeWork defaults on terms as agreed, as I noted in The Tide Is Out and WeWork Bondholders Are Naked:

The applicable landlords could draw under the letters of credit or demand payment under the surety bonds, which could adversely affect our financial condition and liquidity. In addition, under our surety bonds, the applicable surety has the right to request collateral, including cash collateral or letters of credit, at any time the surety bonds are outstanding.

We are also pursuing strategic alternatives to pure leasing arrangements, including management agreements, participating leases and other occupancy arrangements with respect to spaces.

Some of our agreements contain penalties that are payable in the event we terminate the arrangement. In addition, we have limited experience to date with these types of transactions, and we may not be able to successfully complete additional transactions on commercially reasonable terms or at all."

WeWork S-1, 8/15/19

This is why I have speculated that we can't rule out bankruptcy for WeWork as a means to renegotiate its $47 billion in expensive leases even with SoftBank as a parent, which could threaten yet another big hit to SoftBank's WeWork stake as well as existing bonds.

So WeWork will be expensive for SoftBank to take over and help sustain for years, to the tune of billions, which Chairman Son recently acknowledged to SoftBank's investors. "On a call with some of those investors this week, Mr. Son apologized for the WeWork investment, saying he had put too much faith in Mr. Neumann, people familiar with the matter said," according to The Wall Street Journal.

Glad to hear it, but the damage is done. SoftBank's Vision fund is rethinking its risk strategy going forward, with a particular emphasis on improving corporate governance at portfolio companies. Rumors of layoffs at SoftBank and Vision Fund have started to surface amid rumblings of dissent from fund managers who long had voiced concerns about Son's freewheeling investments which now have cost the fund billions in losses with WeWork, Uber (UBER US), Slack Technologies Inc (WORK US), and Zhongan Online P&C (6060 HK). Funding into the new Vision Fund II is at risk as prospective investors have become increasingly wary.

No wonder SoftBank's investors hate this transaction, and this should alarm WeWork bondholders. SoftBank's Tokyo-listed stock is down 30% since the peak in late July just before the WeWork IPO was announced. The CDS spread on SoftBank bonds, which is the cost to hedge against declines, has spiked to the highest level since January.

SoftBank's take over of the catastrophically failed WeWork is a transaction that makes almost no one happy, save ex-CEO Adam Neumann who walks away with $1.7 billion.

Let that sink in.

In the meantime, WeWork bondholders have to take what they get. When and how will WeWork bonds get buried under massive new debt? Don't know. How did the third quarter turn out and what are prospects for the fourth quarter and next year? Probably don't know that either. How long before market analysts and observers move on because one can't adequately cover WeWork's operations or prospects or offer independent valuations for its increasingly illiquid bonds in the vacuum created without publically available financial statements. Not much longer.

As I observed last week to the New York Times, the only good news for WeWork now is that a stronger parent will shepherd it from here:

"SoftBank’s rescue plan has bought some time, analysts said, but WeWork still has to make some difficult decisions. “The silver lining in the whole process is that SoftBank bought them,” said Vicki Bryan, chief executive of Bond Angle, a research firm."

But even this is too little too late.

WeWork 7.875% senior notes lost nearly 7 points to 84.1 (11.9% ytw/1023 bps) since my last report when I had warned again that bondholders should "use any rally as an escape pod." WeWork remains severely distressed and it's not yet clear whether the company can remain viable for the foreseeable future. Existing bonds face the further risk of the company's pending note offerings which will envelop them in a mountain of debt without providing a convincing path for the company's recovery. Upside potential remains limited outside of brief, misguided rallies as a result while downside risk could be 5-10 points from here over the near term. Maintain “Sell.”

Contact Us:

Disclaimer

This publication is prepared by Bond Angle LLC and is distributed solely to authorized recipients and clients of Bond Angle for their general use. In addition:

I/We have no position(s) in any of the securities referenced in this publication.

Views expressed in this publication accurately reflects my/our personal opinion(s) about the referenced securities and issuers and/or other subject matter as appropriate.

This publication does not contain and is not based on any non-public, material information.

To the best of my/our knowledge, the views expressed in this publication comply with applicable law in the country from which it is posted.

I/We have not been commissioned to write this publication or hold any specific opinion on the securities referenced therein.

Bond Angle does not do business with companies covered in its

publications, and nothing in this publication should be construed as a solicitation to buy or sell any security or product.Bond Angle accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this publication and/or further communication in relation to this document.