Tesla Q4: Elon's Burning It All Down

I've long warned 2H this year will mark passing of Tesla's dominance—mainly cuz larger EV mkt is catching up & doing EV better. Fading China sales & Elon's Twitter mess is taking it down even faster.

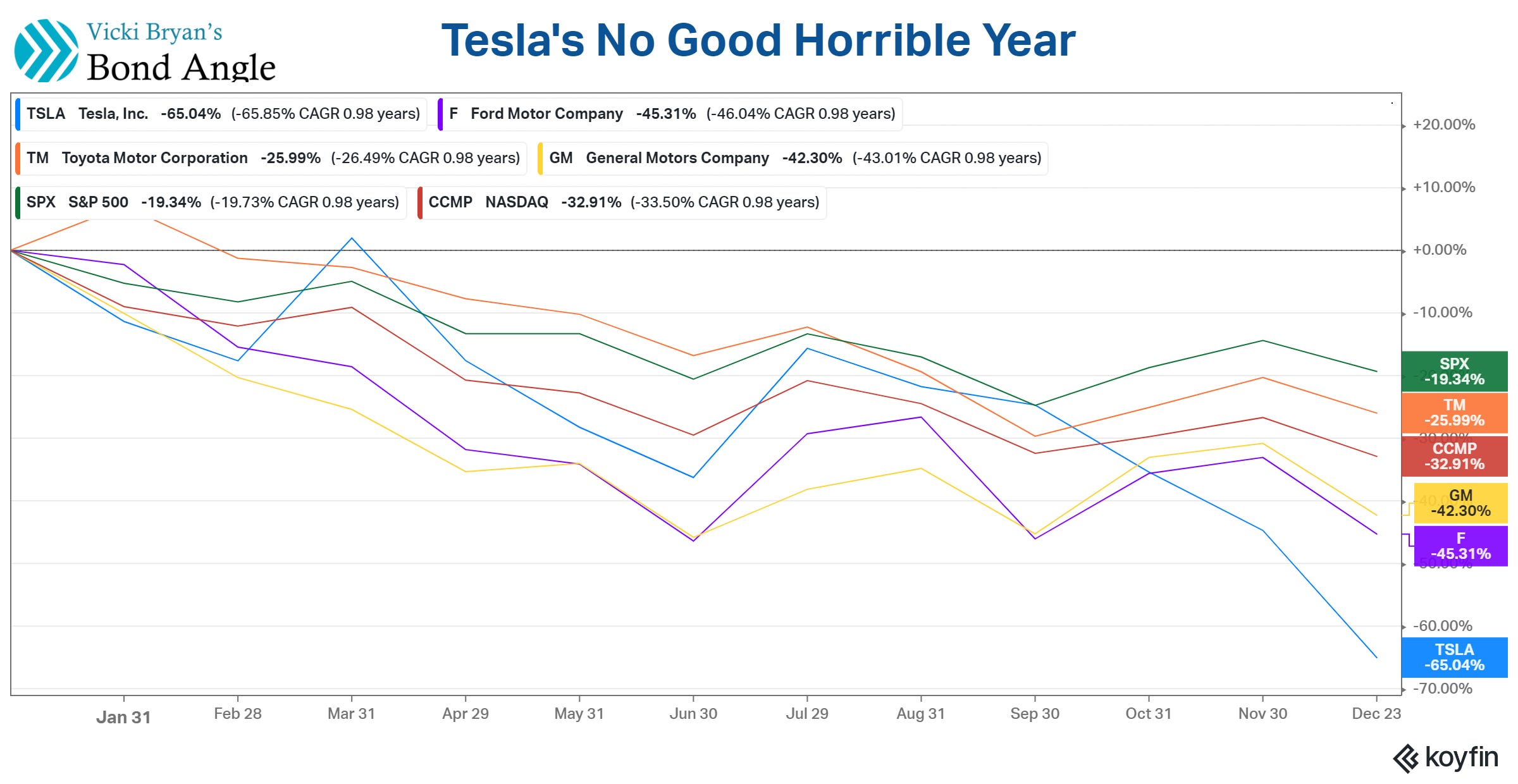

Investors are increasingly alarmed with Tesla TSLA 0.00%↑ stock in freefall, seen trading on heavy volume as low as $109 per share—the lowest since July 2020.

No worries. CEO Elon Musk tweeted to a concerned Tesla investor, a portfolio manager and long time Tesla bull, that he should “Go back and read your old Securities Analysis 101 textbook” where he apparently would learn, Musk lectures, that the decline in Tesla’s stock is actually the Fed’s fault because it increased interest rates to staunch rising inflation:

In simple terms:

As bank savings account interest rates, which are guaranteed, start to approach stock market returns, which are *not* guaranteed, people will increasingly move their money out of stocks into cash, thus causing stocks to drop."

Elon Musk tweet, 12/20/2022

Right. More likely Musk blurted out what he just looked up himself, apparently without really understanding why it’s a nonsensical and exceedingly arrogant deflection that shouldn’t fool anyone in the market, much less a professional money manager and longtime Tesla holder.

First off, investors in Tesla probably didn’t sell their stock to put cash into US bank savings accounts with rates now up to a luscious 0.3%. But even if that is what happened, we would see similar equity market performance to Tesla across the board. We didn’t.

Tesla stock actually attempted a rebound after the Fed’s first rate increase in three years in mid-March, unlike its largest competitors like Ford F 0.00%↑, GM GM 0.00%↑, and Toyota TM 0.00%↑, or the S&P 500 Index, or the NASDAQ .

That brief jump in Tesla stock in March was in line with other EV-makers which all were boosted by the jump in oil prices after Russia invaded Ukraine.

That boost was only enough to offset the bad start of the year for Tesla when it started getting hit with long overdue recalls—nearly 2 million cars recalled through mid-February alone—as well as the start of waves of lawsuits and government investigations into Tesla’s persistent misrepresentations about the feature capabilities and dangerous and recurring flaws in the cars, plus the toxic work environment and dangerous working conditions at its factories—all of which, as I noted at the time, I have detailed for years (as discussed again in Will Tesla Get Good News This Week?, 2/28/22).

Then came April, a very bad month for Tesla stock and the start of its relentless plunge the rest of the year to now two-year lows—a much more severe decline versus its peers or the market.

This happened as investors and market observers came to embrace alarming revelations about Tesla and Elon Musk.

In other words, reality has started to set in.

For those of us paying attention, the writing has been on the wall for years: that Musk is a terrible manager and worse boss (see Dear Elon: There's Nothing Funny About Hitler, 2/17/22) and that Tesla’s fortuitous years of progressive and unchallenged success despite this were probably coming to a close.

And right on time, according to my projections. As I warned, again, this time last year:

Indications are that Tesla’s long stretch of luck and lavish indulgence may be coming to an end. Musk’s billions, brags, insults, and rants have overshadowed growing concerns that can’t be ignored for much longer, like struggling Model 3 same store sales trends I’ve been tracking for years. Like Tesla’s shrinking market share in key markets from robust competition winning buyers spooked by its own notoriously poor build quality in it cars plus its dismal customer service. Like eroding margins from seemingly inflated levels which likely will worsen through next year.

Add emerging consequences from Tesla’s notorious false and misleading full-self-driving (FSD) claims, sneaky “fixes” of serious problems instead of recalls as required, dicey accounting, increasingly significant recalls as years of shoddy manufacturing and apparent coverups are revealed, and escalating government probes may expose all manner of ugliness to the world.

I long have projected that many, if not all of these negative factors may begin to coalesce next year, particularly in the second half. If so, Tesla could struggle increasingly versus record results this year.

Yes, Tesla is closing its best year yet. Or its peak year. We’ll see.

Look Away From Elon Musk To Gauge Tesla's Prospects—and Looming Risks, 12/31/21

You Can See The Peak From Here

Tesla confidently projected continued strong delivery growth in 2022, telling investors in January “we do expect significant growth in 2022 over 2021, comfortably above 50% growth in 2022.”

That lasted one quarter, when first quarter deliveries at 310,048 were up 68% y/y. This tracked the high end of my 300,000-310,000 estimate but trailed even the low end of the projected 312,000-320,000 range of reduced market expectations (see Tesla Q1 Deliveries Come In Under The Wire, 4/2/22).

But trouble was evident when Tesla sales in China plunged y/y through most of the quarter, and more severely versus local peers suffering the same challenging conditions, as I warned in Tesla China Deliveries: Weaker And More Important Than You Think, 3/14/22).

Second quarter deliveries belied normal seasonal trends by falling versus Q1 to 254,695, up just 27% y/y, versus market consensus for 276,000 and my estimate for 251,458 (see Soft Tesla Q2 Deliveries Disappoint on 7/2/22 and Tesla Splitsville on 8/8/22).

This time was harder to explain away, in my view, versus what I saw as accelerating demand weakness as I had expected:

Tesla attributed the severe weakness in the second quarter to extended lockdowns in China as it fought its worst surge yet in Covid-19 cases. True enough but, as I projected back in March, Tesla’s competitors in China faced the same conditions and its toughest rivals still recovered faster and pulled further ahead (Tesla China Deliveries: Weaker And More Important Than You Think, 3/14/22).

BYD Co, for example, reported new record deliveries again in the second quarter, topping more than 100,000 every month while exporting more than twice the cars than Tesla in June.

Critics suggest that BYD numbers aren’t a fair comparison with Tesla with since they comprise sales of full electric (EV) and plug-in hybrid electric (PEV). I would answer that BYD sold 134,000 in June alone, for example, including 70,000 EVs which is nearly what Tesla sold in China over the entire quarter.

Either way, BYD customers chose to not buy a Tesla.

Tesla Splitsville 8/8/22

So I wasn’t surprised when third quarter trends confirmed continued weakness, particularly in China as I had expected, prompting Tesla to initiate what would become several rounds of price cuts and juicy incentives. From Tesla's Q3 Ests Are Fading On Weaker China Sales—Again, 9/27/22:

I expected such competitive pressures on Tesla to continue, and potentially accelerate, when the lockdowns were eased. If so, this comes just as Tesla has essentially doubled production capacity this year via the recently completed expansion of the Shanghai plant plus newly opened plants in Texas and Germany.

Most of China’s exports have been sent to Europe, for example, where Tesla’s market share has been dropping even faster than in China.

Recent reports about Tesla’s shrinking backlog may signal developing confirmation of my concerns. I had noticed that Tesla’s backlog stalled during the production shutdowns. Weird.

If demand remained as robust as Tesla claims, its backlog should have climbed higher. But if I am right about Tesla sinking versus stronger competition in all its markets, that backlog could fall.

Sure enough, Tesla’s backlog has dropped rapidly

And yet investors were blindsided when Tesla’s third quarter results trailed badly versus even rapidly falling market consensus estimates, as I reported in Tesla Q3 Deliveries Trail Even Sharply Reduced Market Consensus—And Its Own Best Guess, 10/3/22:

Tesla reported on Sunday that Q3 deliveries were 343,380. This was up an impressive 42% y/y but trailed managements’ 50% targeted growth rate for the second straight quarter (see Soft Tesla Q2 Deliveries Disappoint on 7/2/22 and Tesla Splitsville 8/8/22).

Deliveries also fell short of tumbling market estimates, again, which had continued to be recast as recently as Friday and still proved to be roughly 20,000-50,000 too high.

Even more troubling was that sales also trailed production for the second straight quarter, this time by a whopping 22,100. That was the highest excess since the 14,176 overproduction in Q1 2020 when the Covid-19 pandemic hit.

This suggests that even Tesla was surprised at the size of the shortfall, coming despite its typical end-of-quarter plug-o-rama; e.g. last minute fleet sales, hurried incentives and discounts, deliberately vague numbers of “cars in transit,” and other maneuverings that usually fill the gaps.

My estimate of 331,104, affirmed last week, was again reasonable close, by comparison, with a difference of 12,700 vs reported 343,380.

By the time third quarter results crashed onto the scene, Musk was soon to close his